Are you a Director confused about whether you need to register for self-assessment? Over the years, HMRC has given conflicting advice when it comes to deciding whether a director needs to register for self-assessment. The result is that this is a much-debated question amongst accountants and Company Directors. So, if you aren’t sure whether you (or your client, if you are an accountant) should be registered, read on.

Friendly Disclaimer: Whilst I am an accountant, I’m not your accountant. The information in this article is legally correct but it is for guidance and information purposes only. Everyone’s situation is different and unique so you’ll need to use your own best judgement when applying the advice that I give to your situation. If you are unsure or have a question be sure to contact a qualified professional because mistakes can result in penalties.

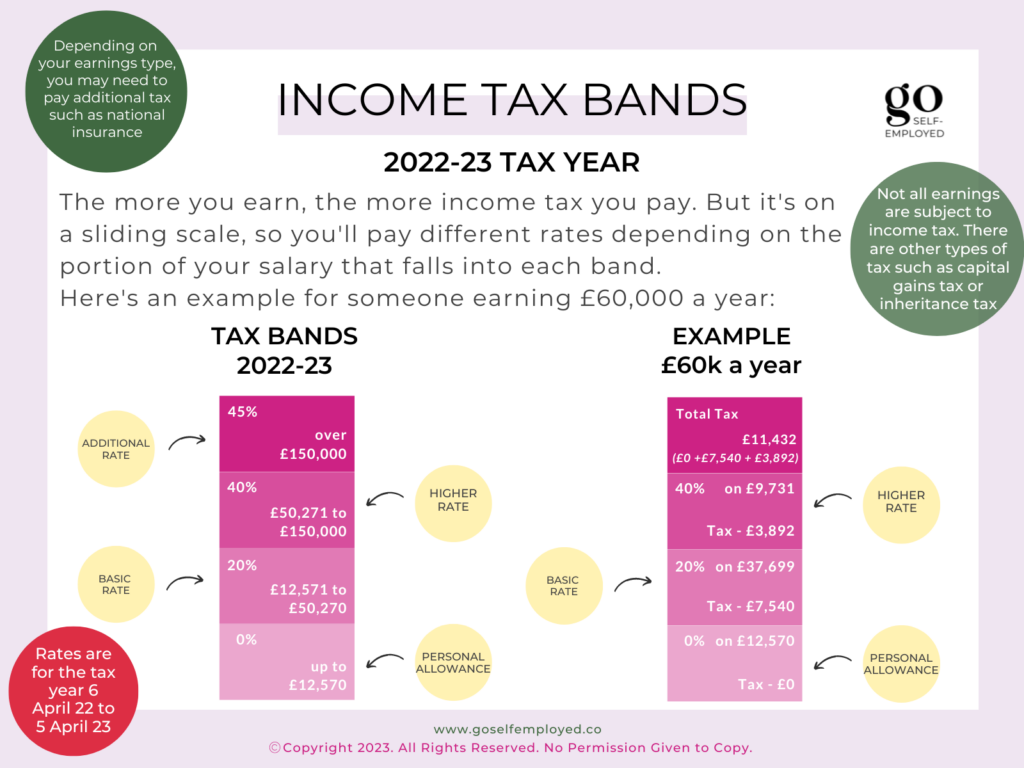

What is Self Assessment?

Self-assessment is a way that UK individuals declare untaxed income to HMRC and pay any tax owed. Currently, they do this using a tax return form, which must be submitted, in most cases digitally, by 31 January each year.

The thing is that a person can be a Director of a Limited Company and not receive any taxable income. So, if they are not receiving any untaxed remuneration, then they have no income to declare on a tax return. In this case, why would they register with HMRC?

The HMRC Rules

According to HMRC legislation, there is no rule stating that a Director must register for self-assessment just because they hold this position. The problem is, years ago HMRC advised that, despite their own legislation, they did want Directors to register for self-assessment and submit a blank tax return, if necessary. The result since then has been that many Directors have continued to register. This has generally to avoid any unwanted attention and hassle if they were investigated.

Should Directors Register for Self Assessment?

A Director in receipt of untaxed income such as dividends should obviously register for self-assessment. This is because they will need to pay tax on this income. The most likely scenario is Director Only Companies. This is where they want to take full advantage of the tax benefit of being incorporated. Plus, pay themselves an efficient combination of dividend and PAYE salary.

But, for Directors who take no salaries, then there is no legal argument that they should register. Indeed, many are now ignoring the recommendation from HMRC and not registering. So, if you are a Director, it’s up to you whether you choose to register. In doing so, you take the risk of HMRC challenging you in the future.

If you are an accountant, then it’s your choice whether you advise your clients to register or not. Some accountants choose to register all their Directors. This is so that each year, they are forced to put the Directors through their in-house annual self-assessment questionnaires. This avoids missing anything that their clients may not have told them about. For example, prompting their clients into letting them know about any untaxed income they may have forgotten about. Or, not realised it needs to be declared on a tax return.

Whatever your situation, registering with HMRC (even if you don’t have untaxed income) could be the safest option to avoid any unwanted attention. But, if you are happy to take on HMRC, then you can choose not to register.

Do Directors Need to Register for PAYE?

A director needs to register for PAYE if they plan to pay themselves with a payslip because they’ll need to deduct income tax and national insurance and report to HMRC. This includes if they pay themselves below the income tax threshold alongside a dividend.

Is a Company Director Self-Employed?

Although you may have formed a Limited Company as a vehicle for your income earned by working for yourself. Legally, you are not self-employed. Your Limited Company is its own entity and you are the Director responsible for running it. You can be an employee collecting a payslip and a shareholder receiving a dividend, where available.

Related: