If you want to stay on top of your numbers for tax-time or find out how your business is performing, then preparing an income and expenditure statement is a great piece of information.

In this guide, I’ll show you how to prepare an income and expenditure statement along with some of the important things you need to look out for when you start adding your numbers and use it to do your taxes. I’ll also give you an example of an Income and Expenditure Statement to further help you.

What is an Income and Expenditure Statement?

An income and expenditure statement is also known as a profit and loss account. Essentially, it summarises all your business income and expenses. It is categorised into different line items such as revenue by type, or costs. For example, freelancers, travel, website costs and marketing.

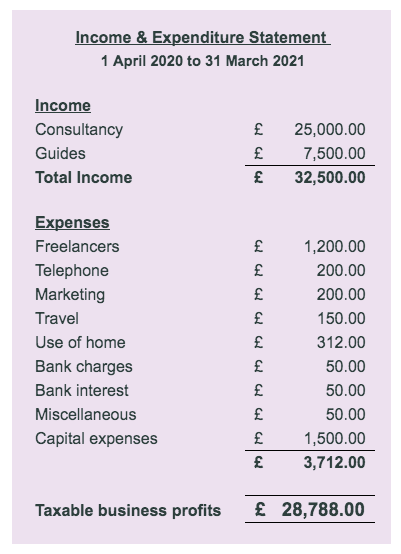

Example of an Income and Expenditure Statement

The statement’s format will vary from business to business because they have different income and expenses. The simplest (and free) way to do one is to use a spreadsheet. Below is an example of an income and expenditure statement for a service based business to help get you started:

When it comes to putting together your own income and expenditure statement, there are a few things you should consider before you start work:

Choose an Accounting Period

You’ll need to have a start date and end date for the timeframe you declare your business income and expenses. This is what HMRC call an accounting period. The easiest dates to choose is either 31 March or 5 April, which matches the tax year. If you choose anything else you could end up with overlap profits and paying more tax than you need to.

Choose an Accounting Basis

HMRC lets you choose between two methods when it comes to deciding which of your business income and expenses you include on your tax return. It’s helpful to decide which one you are using when you prepare your income and expenditure statement so you’ll have the right numbers ready for tax-time. The two methods are:

The cash basis makes your taxes much easier and it is the most popular method with sole traders. It means that registered self-employed business owners with a business turnover of up to £150,000 only include business income and expenses paid during your accounting period on your tax return. By using this method, you’ll only pay tax and National Insurance on the money you’ve received from your clients.

With traditional accounting, you include income and expenses that were invoiced or billed. However, this can make preparing your income and expenditure statement more complicated and time-consuming, especially if DIY-ing your business finances because you’ll need to calculate accounting adjustments like:

- Trade debtors

- Trade creditors

- Accruals

- Prepayments

Is the Cash Basis Right for You?

Categorising Your Income

You’ll only need to give HMRC your total self-employment income, but you may want to break this down if you have different revenue streams. That way, you’ll be able to find out more information, such as where your income comes from or which areas make you the most money. I’ve written a separate guide on tracking your business income, how to set up a system to break it down and common mistakes you need to avoid.

Categorising Your Expenses

There isn’t a right or wrong way to categorising your expenses when you prepare an income and expenditure statement. But, there are a few things you may want to consider:

If you are self-employed and complete the short tax return when you fill in your tax return, then you’ll only need to show your expenses as a single total, without a breakdown. For that reason, you can choose to categorise your expenses in whichever way you feel will be most useful to you. Word of advice though, don’t ‘over categorise’ and create lots of different headings otherwise it will make things too complicated. You can always start with fewer categories and add more as you get more comfortable.

If you fill in the full self-employed section of your tax return, you’ll need to give a breakdown of your expenses to HMRC. For that reason when you set up your income and expenditure statement it may help to use similar business expenses categories as HMRC to make filling in your tax return easier. The categories HMRC uses on the tax return are:

- Cost of goods bought for resale or goods used

- Construction industry – payments to subcontractors

- Wages, salaries and other staff costs

- Car, van and travel expenses

- Rent, rates, power and insurance costs

- Repairs and maintenance of property and equipment

- Phone, fax, stationery and other office costs

- Advertising and business entertainment costs

- Interest on bank and other loans

- Bank, credit card and other financial charges

- Irrecoverable debts written off

- Accountancy, legal and other professional fees

- Depreciation and loss or profit on sale of assets

- Other business expenses

If you want to find out information about your income and spending, then you may want to create categories that you find most useful. For example, there may be certain costs you want to monitor or cut back on for.

Recording Capital Expenses

In business, there are two types of expenses – capital and revenue. Capital expenses are generally the more expensive things than your usual day-to-day expenses. They are for items you use for several years to run your business, for example, a laptop. Revenue expenses refer to your everyday spending, such as subscriptions and bank charges. The way you claim tax relief on capital expenditure is slightly different to revenue expenses and you’ll need to follow the rules of capital allowances.

Businesses use capital allowances to claim tax relief on capital expenses set out by HMRC. But, if you choose the cash basis for accounting, then you’ll be able to claim the full amount you’ve paid in the tax year you buy it. Also, most businesses, whether they choose cash or traditional accounting, can claim the annual investment allowance. That gives them full tax relief in the tax year they make the capital expenditure but this needs to be claimed separately on their tax returns.

Calculate Your Profit

Your profit is the difference between your income and expenses, and it is this figure you will pay tax on. Remember, not all your business expenses will be tax-deductible, even if you pay for them as part of running your business. These are known as disallowable expenses and include:

- Fines and penalties, e.g. parking fines

- HMRC interest and penalties

- Training and courses for new skills

- Food, except in certain circumstances

- Personal expenses

- Drawings

You can find out more about allowable business expenses in my separate guide, including claiming for mileage and use of home. If you’re newly self-employed, don’t forget to check this guide to find out whether you can claim any pre-trading expenses.