P11d Vans and Van Fuel Section G covers details of company vans and van fuel made available to employees for their own private use.

P11d Vans and Van Fuel provided fall under section G of the P11d form.

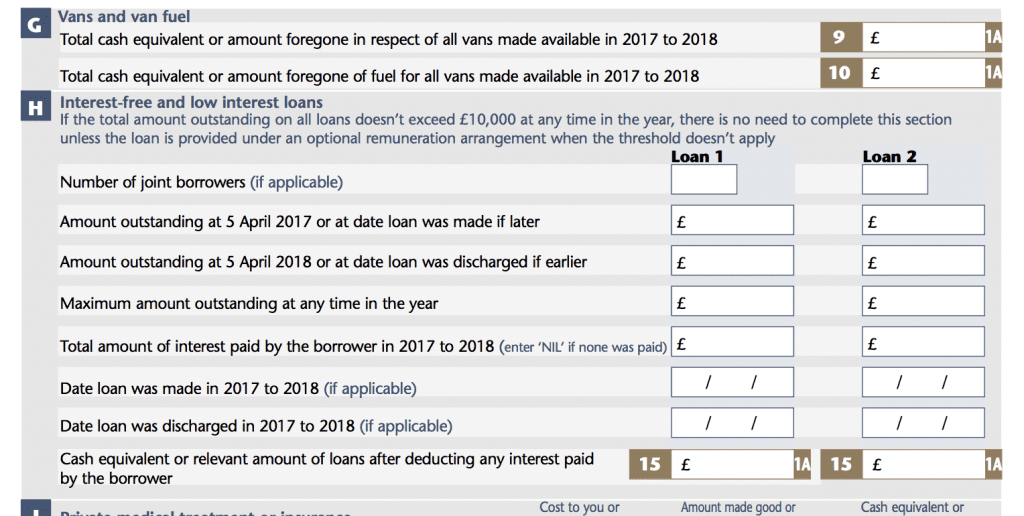

The P11d value to input in boxes 9 and 10 of the P11d form is a fixed amount set by HMRC, regardless of van price or private fuel usage.

P11d Van and Van Fuel Benefit Rates

HMRC set out fixed amounts that need to be used for P11d purposes for vans and van fuel. These are:

| 2022-23 | 2021-22 | 2020-21 | 2019-20 | 2018-19 | 2017-18 | |

| Van Benefit | £3,600 | £3,500 | £3,490 | £3,430 | £3,350 | £3,230 |

| Van Fuel Benefit | £688 | £669 | £666 | £655 | £633 | £610 |

So for any vans and van fuel provided, you simply need to input these figures onto the P11d forms.

HMRC Definition of a Van

HMRC have strict rules that determine whether a vehicle is classified as a van or a car for P11d purposes.

The HMRC definition of a van is:

- a vehicle of a construction primarily suited for the conveyance of goods or burden of any description (this doesn’t include people);

- with a design weight (the weight which the vehicle is designed or adapted not to exceed when in normal use and travelling on a road laden) not exceeding 3,500 kilograms.

For double cab pickups, HMRC sets a further rule that vans of this type must have at least a one-tonne payload (including any hardtop lids), otherwise, these will be classified as a car.

Employee Contributions

If an employee makes a contribution towards the cost of the van for their private usage, then you need to deduct any contribution made pound for pound against the HMRC benefit rates.

P11d Value of Zero Emission Vans

HMRC sets out special rules for zero emission vans meaning that the van benefit charge can be reduced by a fixed percentage before you enter it onto the P11d form.

The percentage reductions are:

| 2017/2018 | 2018/2019 | 2019/2020 | 2020/2021 | 2021/2022 |

| 20% | 40% | 60% | 80% | 90% |

So for example, for 2018/2019 the P11D Benefit for a Zero Emission van would be £1,340 (40% x £3,350).

Van Fuel Benefit

Van fuel benefit must be paid where a van is used for personal journeys unless those journeys are ‘insignificant’.

An insignificant journey is one that is small and doesn’t take up much time in the year, HMRC is not prescriptive about its definition of insignificant so always seek professional advice to confirm how to classify your usage.

Here are some examples to consider:

- A week’s exclusive private use is not insignificant;

- Doing weekly supermarket shopping in the company van is not insignificant;

- Taking the van on holiday is not insignificant;

- Using the van for social activities is not insignificant;

- A slight detour to the newsagent is insignificant;

Who Pays Tax for P11d Vans and Van Fuel Section G

Tax on van and van fuel included in Section G is paid by the employee and Class 1a National Insurance payable by the employer.

For example if an employee pays tax at 40%, then for 2017/2018 they will need to pay:

Van Benefit £3,230 x 40% = £1,292

Van Fuel Benefit £610 x 40% = £244

The employer will pay Class 1 a national insurance at 13.8% on both the van benefit and van fuel of £ 529.92 (although this attracts business tax relief).