Paying yourself tax efficient Directors from your Limited Company will achieve savings for both you and your business. As a director, you have to make the right decisions how to pay yourself. Although this often means having greater flexibility over how you do this, it can also potentially determine reduced tax payments, depending on your situation. Here, you’ll find out the optimum directors salary for 2022/23 to maximise tax savings. If you’re a director and wondering how to pay yourself from your Limited Company, it’s a good idea to bookmark this page so you can use it as a reference.

Friendly Disclaimer: Whilst I am an accountant, I’m not your accountant. The information in this article is legally correct but it is for guidance and information purposes only. Everyone’s situation is different and unique so you’ll need to use your own best judgement when applying the advice that I give to your situation. If you are unsure or have a question be sure to contact a qualified professional because mistakes can result in penalties.

1. How To Pay Yourself from Your Limited Company

Accountants commonly recommend that owners of a Limited Company pay themselves a combination of minimum Directors salary through PAYE and dividend. That’s because it minimises both Personal Tax and Corporation Tax by taking advantage of tax-free and lower tax rates available from these four taxes – income tax, dividend tax, corporation tax and National Insurance.

2. What is the Optimal Directors Salary for 2022/23?

If you have a Director Only Limited Company, then the optimal directors salary for 2022/23 is £758 per month or £9,100 per year. But everyone’s circumstances are different and this is based on the following assumptions:

- You are the sole employee of your Limited Company and are not entitled to claim the employment allowance;

- If you have no other forms of taxable income and adjustments for your taxes;

- You earn less than £100,000 and are unaffected by the personal allowance restriction

- You’re on the standard tax code for 2022/2023 of 1257L

If you employ staff on your payroll who aren’t Directors, then the most tax efficient directors salary 2022/23 is £992 per month or £11,904 per year.

Always consult a professional to discuss your personal situation and help deciding on the optimum director’s salary for you.

2.1 How is the Directors Minimum Salary 2022/23 Calculated?

The directors minimum salary for 2022/23 of £758 takes advantage of tax-free income tax and National Insurance limits. When directors salaries are paid via a payslip, their pay becomes subject to income tax and National Insurance.

The income tax rates for 2022/2023 are:

- £0 to £12,570 0% (personal allowance)

- £12,571 to £50,270 20% (basic rate)

- £50,271 to £150,000 40% (higher rate)

- Over £150,000 45% (additional rate)

National Insurance rates applicable to payslip salaries for 2022/23 are:

- Primary threshold where you start paying NI £533 per month or £6,396 for the year;

- Secondary Threshold where Employers start paying NI £823 per month for 1 April to 30 June 2022 and then £1,047 per month for 1 July 2022 to 31 March 2023;

- Lower Earnings Limit where you do not pay NI but credit for the benefits of doing so like the state pension, £758 per month or £9,100 for the year.

Based on the rates above, it makes sense for UK Directors to take a salary that protects their access to state benefits but avoids paying National Insurance both as an employer or employee at the lower earnings limit – so that’s £758 per month. It’s also below the personal allowance limit so avoids income tax. Additionally, any PAYE salary Directors pay themselves is a tax allowable expense so saves corporation tax.

2.2 How are Dividends Taxed?

A dividend is money that you take from your Limited Company from profits after Corporation Tax. It is not a tax allowable expense.

The first £2,000 taken is tax-free as it is covered by the dividend tax allowance and any remaining dividends are taxed as follows:

| Dividend Tax Rates | Income Tax Rates | |

|---|---|---|

| £0 to £12,570 (personal allowance) | 0% | 0% |

| £12,571 to £50,270 (basic rate) | 8.75% | 20% |

| £50,271 to £150,000 (higher rate) | 33.75% | 40% |

| Over £150,000 (additional rate) | 39.25% | 45% |

When you compare the dividend tax rates to income tax rates, you can see that the dividend rates are lower. For example, as a basic rate taxpayer, you’ll pay 8.75% on income taken as a dividend instead of 20% income tax. So, the optimum mix of salary v. dividend minimises Directors tax bill by letting them take advantage of lower tax rates.

Always consult a professional to discuss your personal situation and help deciding on the optimum director’s salary for you.

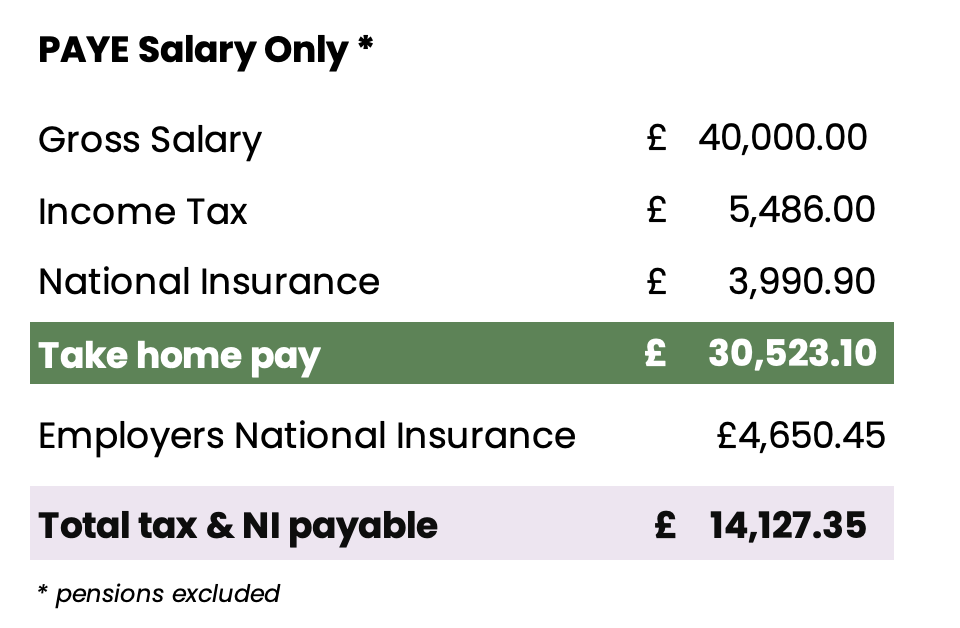

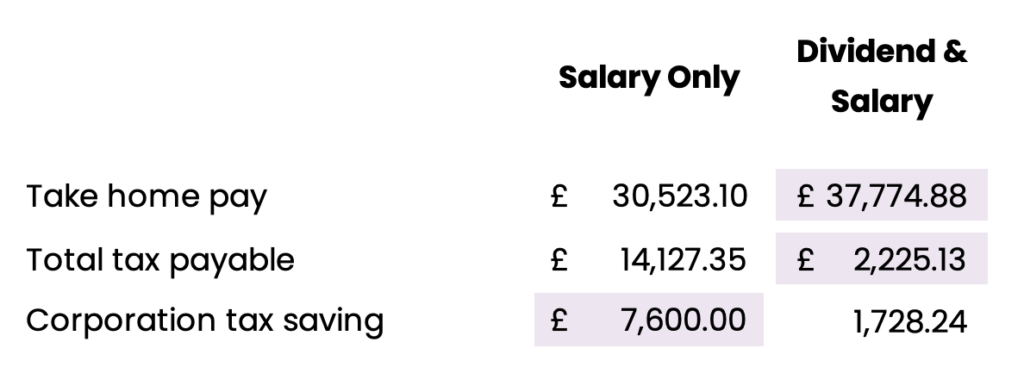

3. Example of Tax Efficient Directors Salary 2022/23

Let’s assume you want to pay yourself £40,000 from your Limited Company. Paying yourself £40,000 through payroll will result in tax of £14,127.35. However, by using the optimum mix of dividend and salary you’ll pay £2,225.13 in tax and benefit from an extra £7,251.78 take-home pay. Here are the calculations:

4. Final Thoughts on Taking The Tax Efficient Directors Salary 2022/23

Although the optimal directors salary for 2022/23 is tax efficient, it’s also worth remembering that:

- To pay your Directors salary, you’ll need to register as an employer so you can issue yourself a payslip and report your pay to HMRC under the rules of RTI;

- You cannot take a dividend if your business makes a loss or there are insufficient reserves on the balance sheet;

- You can pay yourself a salary even if your business makes a loss;

- Dividends are not salary so may not be accepted by mortgage lenders as part of providing evidence of your income;

- Depending on your plans you may need to pay yourself more than the optimal Directors salary of £758 per month. For example, if you need to present a payslip to apply for a mortgage;

- In the recent Covid-19 crisis, many Limited Company owners found themselves unable to claim furlough to match their income because dividends did not count as salary.

Related: