The tax point of an invoice is the date used for VAT purposes to determine the date that VAT must be charged, and which VAT quarter it gets included in. Tax points may vary from invoice to invoice. Here are the most common scenarios, the tax point to use and an example of the tax point..

Updated 28 July 2021

Table of contents

1. What is a Tax Point?

A tax point is the date that VAT falls due on a product or service that has been sold. Sometimes in business, transactions aren’t straightforward. For example:

- They may be broken down into phases or;

- There may be delays between closing off a project, delivering an item and raising an invoice.

HMRC sets out rules determining what date you must use as the tax point on an invoice. That means it can alter which VAT quarter a sales invoice gets included in. Here are the most common scenarios and how to determine the tax point for each:

- Accepting cash, no invoice needed, the tax point is the date of supply**;

- VAT Invoice issued 15 days or more after date of supply **, the tax point is the date the supply took place;

- Payment or invoice issued made in advance of supply, the tax point is the date of payment or invoice whichever is earlier;

- Payment in advance of supply and no VAT invoice yet issued, the tax point is the date payment was received.

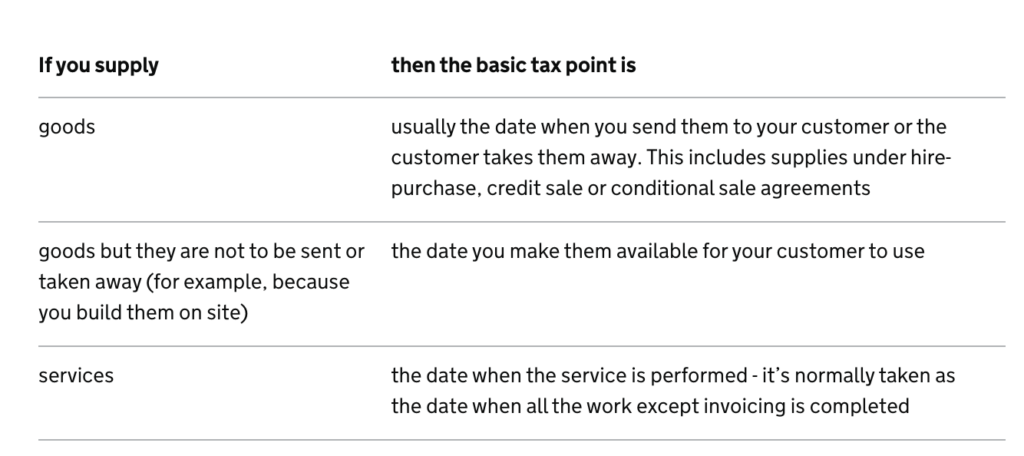

**Date of supply means:

- for goods: the date they were sent, collected or made available to the customer;

- for services – the date the work is completed

2. What is a VAT Invoice?

A VAT invoice contains certain information legally required by VAT registered businesses. This is in addition to the usual invoice information such as customer address, the amount payable and bank details, additional VAT information needs to appear:

- VAT rate being used;

- What VAT is charged;

- VAT Registration number;

- the total amount owed including VAT.

You can find a VAT invoice template here.

3. Example of the Tax Point of a VAT Invoice

A self-employed gardener orders new some new equipment at a total cost of £2,500 plus VAT. She pays a deposit of £500 and pays the balance upon delivery. In this example there are two VAT tax points:

- The date the deposit is paid, which includes VAT of £83.33 (calculated as £500 x 20/120)

- The date that the goods are delivered, which includes VAT of £416.67

The supplier of the gardening equipment would need to include the two amounts of VAT in the VAT quarters they fall on an individual basis.

4. Tax Point of an Invoice and the Cash Accounting Scheme

The VAT cash accounting scheme is one of the many VAT schemes available from HMRC which permits businesses to pay VAT on invoices and claim back VAT on expenses according to when they pay for them. For businesses using cash accounting, the tax point of a VAT invoice is always the date the payment is received.