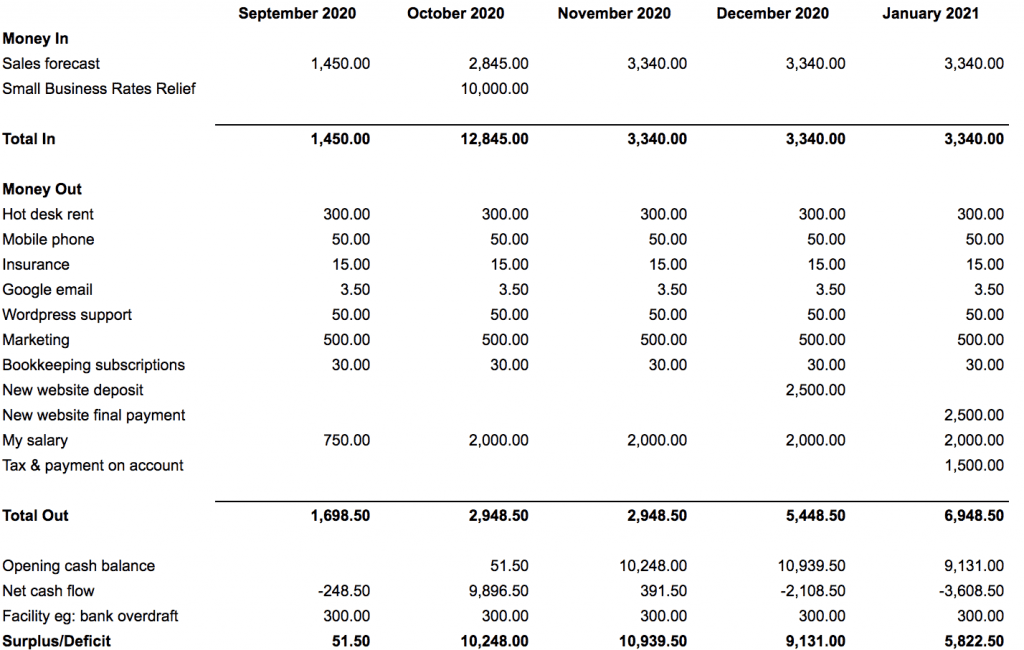

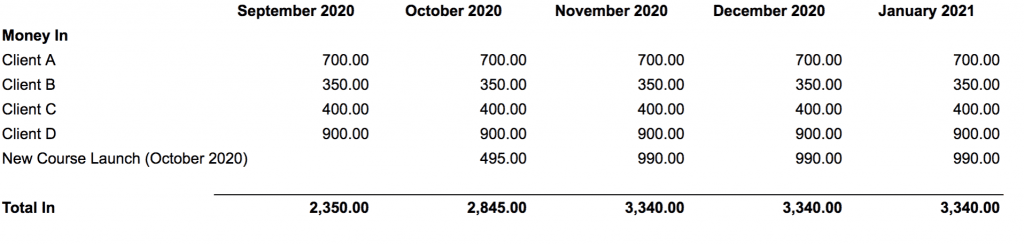

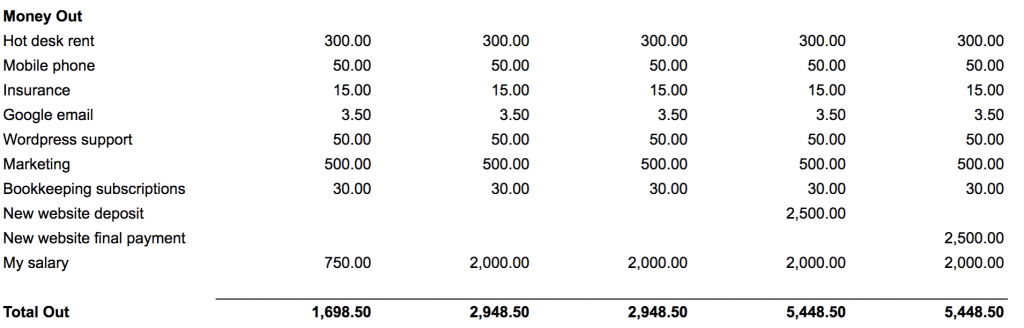

A cash flow forecast shows you how much money is coming into your business, where it is being spent and whether you have enough money in the bank to pay your bills (and pay yourself). It’s also very useful to give you a heads up if any problems are coming your way. In this guide, I’ll share my simple cash flow forecast template and walk you through how to fill it in, as well as how to review the numbers.

Don’t worry, you only need basic spreadsheet skills! And I’ll use a cash flow forecast example to help.

’

–

’

’

’ ’ ’

’’

’

’’’

’

’

’’

’

’

’

’

££

’

’

’’’

’

–’’

£

’