Doing your accounts is just one of the many moving parts of running a business when you’re self-employed.

If you’re a sole trader and bookkeeping means nothing to you or you keep trying to put together spreadsheets but get stuck on what to include, then this guide will be helpful to you.

I’ll run through the process of bookkeeping for self-employed folks. I’ll start with the basics of what you need to be tracking ( and why), explain the different platforms you can use and make some suggestions to help guide you through deciding what platform is right for you.

And finally, I’ll show you an example of how to do your own accounts when you’re self-employed using a spreadsheet.

Don’t forget if you have a question on this guide or any of my others, you’ll find me inside my Facebook group – The Self-Employed Club.

Table of contents

I use affiliate links on my website for products I know, love and (mostly) use myself. It means that I may earn a small commission when you use my links and make a purchase, without incurring additional fees yourself.

Bookkeeping for Self-Employed Folks

Before we start getting into the details of HOW to do your bookkeeping, it’s helpful to understand WHY you need to do it.

What is Bookkeeping?

There are lots of different definitions of bookkeeping for sole traders. Here’s mine:

Bookkeeping means keeping a record of all the money that comes in and out of your business with all the right numbers grouped together, to help:

- Make filling in your tax return easier;

- Keep a record of how you reached the numbers you put on your tax return;

- Track how much tax you owe;

- Gauge what’s happening inside your business.

From a legal perspective, when you are self-employed, you don’t actually send your accounts to HMRC. You’ll just enter details of income and expenses onto your return.

How to Do Your Own Bookkeeping

When it comes to doing your own accounts, there are two ways you can do it:

- On a spreadsheet

- By signing up for an accounting software

Currently, unless you are VAT registered, you can choose to use either. But from 6 April 2026, HMRC will require self-employed business owners with a business turnover of £50,000 or more to use an accounting software and submit quarterly self-assessment tax returns via the platform.

These changes are part of making tax digital and the turnover threshold will drop to £30,000 from 6 April 2027 to include more people.

Using a Spreadsheet for Your Self-Employed Accounts

A spreadsheet is a popular option for doing self-employed accounts – there are no monthly subscription costs or complicated software to get to grips with.

Using an Accounting Software for Self-Employed Accounting

Although some are available for free, most are bought through a monthly subscription, like Xero. Once subscribed you simply sign in, do your bookkeeping and the system will store all your data and generate reports about your business as well as for your filling in your tax returns.

Spreadsheet or Accounting Software? What’s Right?

Using a spreadsheet is an easy way to get started tracking your income and expenses, especially if self-employment is new to you. But as your business grows using a spreadsheet to handle a large amount of data things can get tricky and time-consuming.

If you feel confident or your business is growing quickly you may want to go for an accounting software. I use Xero for my bookkeeping and the monthly fee covers invoicing, handling foreign currency transactions and pulls transactions straight from my business bank account.

Remember from April 2026 the switch to an accounting software may be inevitable depending on your business turnover, but starting with a spreadsheet is a nice way to introduce yourself to the basics of business finance without needing to learn how to use an accounting software if self-employment is new to you.

How to Do Your Own Accounts When You’re Self-Employed (+ an Example)

You’ll need to set up one spreadsheet for each tax year* that way you have everything you need for your tax return in one place.

* The tax year runs from 6 April to 5 April each year.

#1: Open a Business Bank Account

If you haven’t, opening a separate business bank account will make your bookkeeping easier because all your income and expenses will be in one place. It’ll save you sifting through your personal account transactions searching for your business transactions.

I’ve used Wise for a number of years now because I have foreign currency transactions and love it, but Starling is really popular amongst sole traders as well.

#2: Open Google Docs or Excel

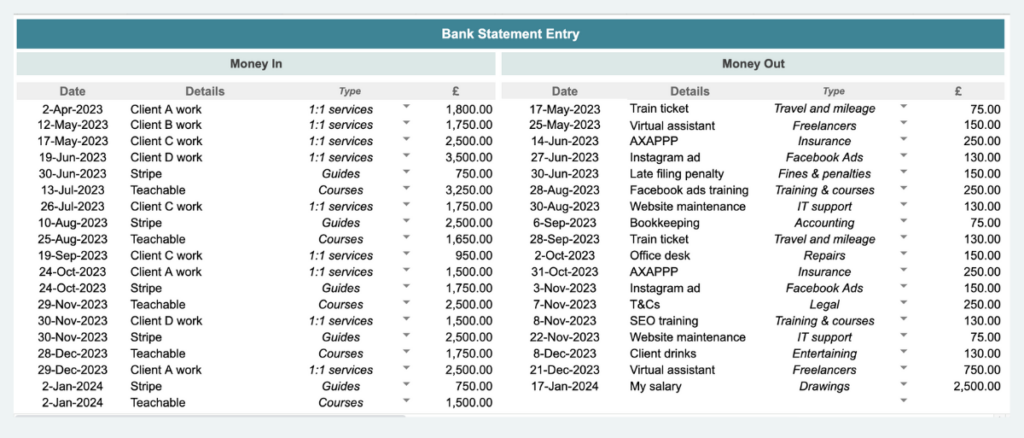

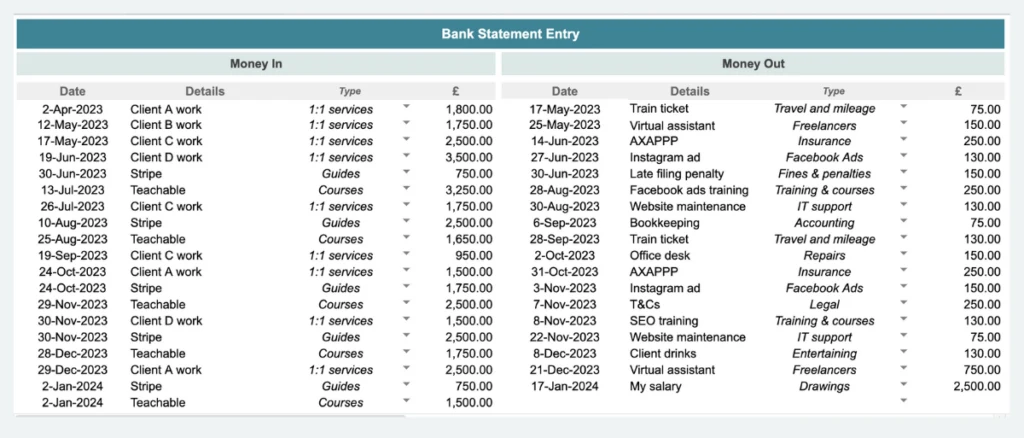

Create a tab to enter your income and expenses from your bank statement, with the columns:

- Date

- Detail

- Type of Income/Expense

- Amount (£)

#3: Decide on Your Income and Expense Categories

Grouping transactions together will give you a clearer picture of what you are spending money on and what areas make you the most money. Choose the most suitable categories for your business.

I recommend you keep it simple when it comes to choosing your categories and only create the ones you really need. Otherwise, it could make it complicated for you to review your numbers and do your tax return.

#4: Choose Your Start Date

The easiest choice is to pick a start date that matches the tax year (6 April to 5 April). HMRC accepts 1 April to 31 March as being the ‘same’ as the tax year, which can make things easier to think about.

You can choose another start date of your choice but this may have tax implications so speak with a professional to understand the impact of using another date for you.

#5: Add the Numbers from Your Bank Statements

Transfer the numbers from your bank statements starting from the start date you chose in #4, filling out the details on your spreadsheet along with the categories. Make sure your spreadsheet adds the totals for your income and expenses as you go along.

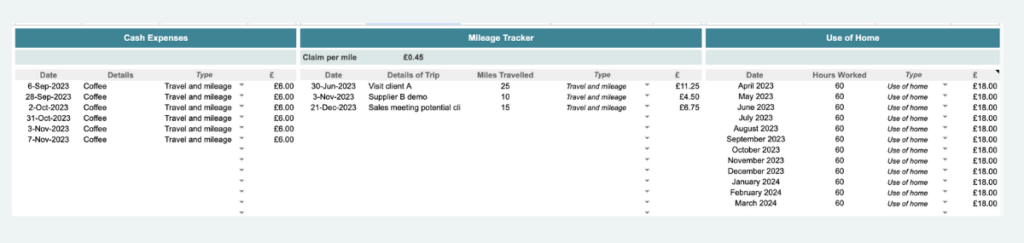

#6: Include Tax Allowable Expenses Not On Your Bank Statement

There may be certain expenses that don’t have receipts or things you have paid for outside of your business bank account, like in cash or from your personal bank account. Make sure you include these and store the receipts so that you can claim all the tax relief you’re entitled to, which may be:

- Mileage when you use your personal vehicle;

- Working from home.

#7: Calculate Your Profit and Estimate Your Tax

Take the totals from your income and expenses sheet and calculate your business profit. That will tell you how much money you’ll pay tax on so you can make an estimate of what you owe.

Don’t forget to set aside your tax money so you don’t spend it – both Wise and Starling have the option to set up pots to help ring-fence money away from your current account.

Hopefully, you now have a better idea about how to do your own accounts if you’re self-employed and the options available.

Remember these 3 important things:

- It’s fine to start simple with a spreadsheet to build your confidence with business finances

- Set aside time to do your bookkeeping regularly

- Make sure you estimate your taxes and set aside the money

Looking for a done-for-you bookkeeping spreadsheet? I’ve created a bookkeeping spreadsheet for the UK self-employed which takes care of all the complicated formulas, estimates your tax bill and adds up your numbers ready for your tax return.

GET MY BOOKKEEPING SPREADSHEETKeep Reading and Learning: