Using the cash basis for tax returns is a popular choice for sole traders because it can make bookkeeping and filling in their tax returns quicker and easier, especially if they are using a spreadsheet.

Keep reading to find out all about the cash basis for tax returns, who is allowed to use it and the pros and cons of doing so.

Friendly Disclaimer: Whilst I am an accountant, I’m not your accountant. The information in this article is legally correct but it is for guidance and information purposes only. Everyone’s situation is different and unique so you’ll need to use your own best judgement when applying the advice that I give to your situation. If you are unsure or have a question be sure to contact a qualified professional because mistakes can result in penalties.

What is the Cash Basis for Tax Returns?

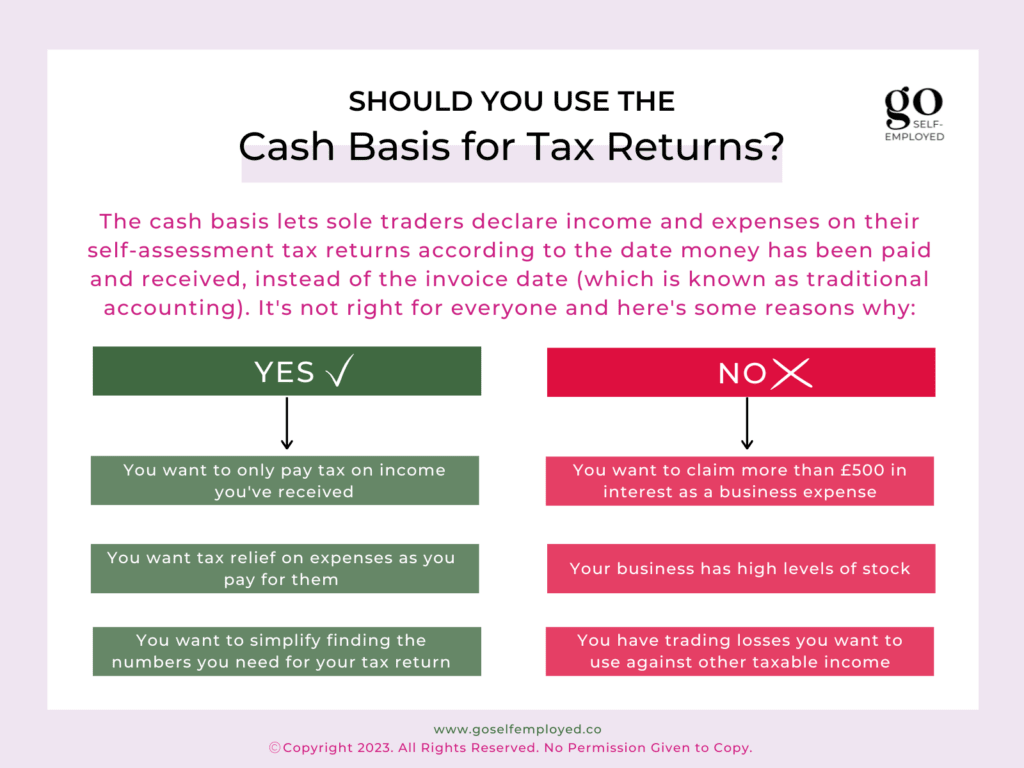

Using the cash basis means you declare your income and expenses which you have actually been paid on your tax return. As a result you’ll only pay tax and national insurance on the money you’ve received from your clients and customers.

The alternative to the cash basis is traditional accounting where you include income and expenses that were invoiced or billed. This can make preparing your income and expenditure statement more complicated and time-consuming that needs be, especially if your tax affairs are fairly simple.

Who Can Use the Cash Basis?

Only sole traders with a turnover of £150,000 or less during an accounting period can use the cash basis. (or £300,000 if claiming universal credit). Once you have chosen to use the cash basis, you can continue to use it until your business turnover reaches £300,000.

Who Can’t Use the Cash Basis?

There are some very specific groups who cannot use the cash basis including:

- Lloyd’s underwriters

- farming businesses with a current herd basis election

- farming and creative businesses with a section 221 ITTOIA profit averaging election

- businesses that have claimed business premises renovation allowance

- businesses that carry on a mineral extraction trade

- a business that have claimed research and development allowance

- limited companies

- limited liability partnerships

- dealers in securities

- relief for mineral royalties

- lease premiums

- ministers of religion

- pool betting duty

- intermediaries treated as making employment payments

- managed service companies

- waste disposal

- cemeteries and crematoria

(Source: HMRC)

Should You Use the Cash Basis for Your Tax Return?

It depends, here are some of the pros and cons of using this method:

Pros

The cash basis is a really popular option with sole traders. It is commonly chosen by those that are handling their own taxes because:

+ You’ll only pay tax on income that you’ve been paid. Therefore, if you have a slow-paying client, you won’t pay HMRC until you get paid.

+ You avoid dealing with capital allowances (except for cars), meaning you get full tax relief for any major expenses in the tax year you pay for them.

+ It makes preparing your income and expenditure statement much easier because you can use your business bank statements to find your income and expenses, instead of going through your invoices.

Cons

Despite some clear advantages, the cash basis isn’t always right for everyone. Some people opt to use traditional accounting instead of cash accounting when:

- They want to claim interest or bank charges of more than £500 as an allowable business expense;

- Their business has high levels of stock;

- They have trading losses you want to offset against other taxable income;

- They want their income and expenditure statement to reflect the true profit of their business. For example, if they’ve paid for expenses upfront for a job that their client hasn’t paid them for during the tax year.

Cash Basis v Traditional Accounting

The accounting method that is right for you really depends on your personal circumstances. Let’s suppose that during the tax year 2022-2023 you invoice a customer £2,000 and they part paid your invoice sending you £1,000.

Using the cash basis, you would only include £1,000 in your income on your tax return. But, using traditional accounting you’d need to show the full £2,000 and pay tax on this.

However, let’s say you are setting up your business and have been invoiced £5,000 for your new website. You’ve only paid £2,500 to your web developer during the tax year 2022-2023, agreeing to pay the balance at some point during 2023-24.

Using the cash basis, you would claim £2,500 as an expense in 2022-23 and the rest in the subsequent year. However, with traditional accounting, you’ll be able to claim the invoice value of £5,000 in one tax year. This means you get the tax benefit sooner rather than later.

Can You Switch Between the Cash Basis and Traditional Accounting?

You can change from the cash basis to traditional accounting between different tax years, but you must use the same one for each complete accounting period. You also must have a reason for making a change such as using tax losses. If you want to switch between the two, you need to make sure you make adjustments to the numbers you put on your tax return. This is to ensure you don’t double count or omit income and expenses.

HMRC have a worksheet you can use to help you calculate the adjustment you need to make on your tax return.

Any losses generated by a business changing from the traditional to cash basis can only be carried forward. They cannot be used as sideways relief against other income or be carried back against earlier year’s profits.

Offsetting Tax Losses Under the Cash Basis

The cash basis, for some, doesn’t just reduce their tax bill it even creates a tax loss. But, to keep things fair between everyone who is self-employed, HMRC has rules on how these losses can be used:

- Losses cannot be set off against other income except for your self-employment profits, known as sideways relief;

- Losses cannot be carried back and set against any previous years income;

- Terminal losses must be set against any profits (after deducting losses brought forward) from the same business being taxed in the year;

- Any remaining terminal losses must be set against the profits of the same business taxed in the 3 prior years, starting with the latest year

Related: