Capital allowances affect how you claim tax relief on certain types of expenses in your business when you fill in your self-employed tax return. In this guide, you’ll find out what HMRC capital allowances are and what types of expenses are covered by the rules. I’ll also show you how to claim them on your tax return.

Table of contents

- 1. What are Capital Allowances?

- 2. How Much Are HMRC Capital Allowances Rates?

- 3. How Capital Allowances for Cars Work

- 4. How to Claim Self-Employed Capital Allowances on Your Tax Return

- 5. Capital Allowances v Depreciation

- 6. Capital Allowances v Annual Investment Allowance

- 7. What is the Capital Allowances Super Deduction?

Friendly Disclaimer: Whilst I am an accountant, I’m not your accountant. The information in this article is legally correct but it is for guidance and information purposes only. Everyone’s situation is different and unique so you’ll need to use your own best judgement when applying the advice that I give to your situation. If you are unsure or have a question be sure to contact a qualified professional because mistakes can result in penalties.

1. What are Capital Allowances?

Capital allowances affect how you claim tax relief when you buy more expensive items for your business. These are things that you will use for a number of years such as:

- Laptop, computers and printers

- Office furniture

- Equipment

- Tools

These types of expenses are what are known as capital assets in accounting.

1.1 How Self Employed Capital Allowances Work

Say you buy a laptop for £1,500 and intend to use it for 3 years. In accounting, we would need to claim tax relief for the cost of the laptop over the same period of time we intend to use it. So, in this case, we would need to claim £500 as an allowable expense on your self-employed taxes over 3 years.

What this meant was that self-employed business owners reduced the number of years they said they were going to use equipment to accelerate their claim against their taxes. In order to equalise things in the sole trader community, HMRC brought in capital allowances. This is where they set out fixed percentage tax relief that all business owners must use a business claim each tax year, depending on what type of assets they have bought.

1.2 Capital Allowances and the Cash Basis for the Self-Employed

If you choose to use the cash basis when it comes to filling in your tax return, then you can ignore the rules of capital allowances unless you have bought a car through your business. You just claim the cost of what you have bought alongside your other allowable business expenses.

2. How Much Are HMRC Capital Allowances Rates?

There are three main categories of capital allowances, which you must use depending on the type of assets you have bought. These three categories exclude cars, which are treated slightly differently (see below). Here’s how much businesses can claim as a percentage of the cost of the capital asset they have purchased on each tax return:

2.1 Main Rate Pool – 18%

This pool includes things like plant & machinery, equipment and furniture.

2.2 Special Rate Pool – 8%

This is a unique category and refers to purchases which are:

- parts of a building considered integral – known as ‘integral features’;

- items with a long life of over 25 years;

- thermal insulation of buildings;

- cars with CO2 emissions of more than 130g/km.

2.3 Single Asset Pool – 18% or 8%

A business can create a single asset pool where an asset that has a really short life but you cannot include in this pool any cars, special rate items (number 2 above) or anything that you use for non-business reasons.

3. How Capital Allowances for Cars Work

Business claim for HMRC capital allowances on cars based on CO2 emissions of the vehicle and whether it is new or second hand. Here are the applicable rates:

[table id=28 responsive=scroll/]

Here’s an example:

You buy a car for £10,000 and use it for 70% business. The car has emissions of less than 50 g/km. You can expense the full business amount of the car – £7,000 (£10,000 x 70%) against your taxes in the tax year you buy it. If the same car had emissions of 120 g/km then you’ll work out the amount you claim as an allowable business expense differently.

Tax Year 1

Cost of car 10,000

Claim 8% 800 (business use claim on your tax return is £560)

Cost c/fwd 9,200

Tax Year 2

Cost of b/fwd 9,200

Claim 8% 736 (business use claim on your tax return is £589)

Cost c/fwd 8,464

You’ll then need to keep going year on year until you either sell the car (and need to make a balancing adjustment) or you have claimed for the full amount of the car against your taxes, whichever comes first. Depending on which car you have in mind the amount you can claim will vary.

4. How to Claim Self-Employed Capital Allowances on Your Tax Return

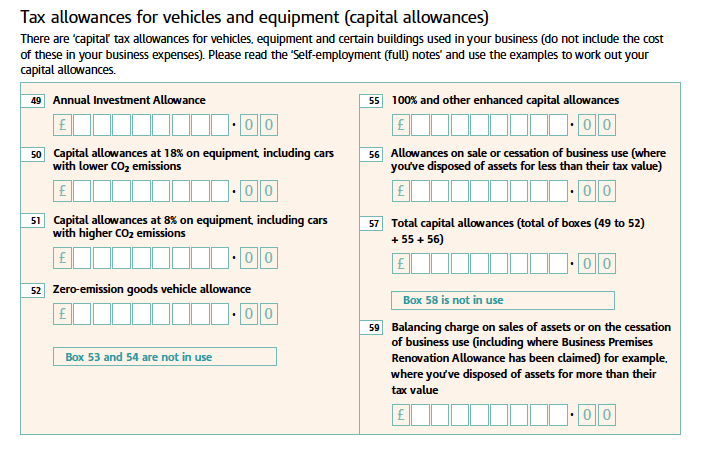

You’ll need to claim your capital allowances in boxes 50 to 59 in the self-employment section of your tax return. You can choose to show depreciation, but this will be flagged as a disallowable expense and added back when calculating your business profits.

Whatever your business turnover, you should keep a note of the self-employed capital allowances you are claiming for and how you worked it out as part of your business records. This is in case of an HMRC investigation and they ask for evidence of what you are claiming for to check you’ve paid the right amount of self-employed tax.

5. Capital Allowances v Depreciation

Depreciation is an accounting adjustment made to spread the cost of an asset over the life in the income & expenditure statement or accounts of a business. Since every business will spread the cost differently, to avoid one business claiming more tax relief than another, depreciation is treated as a disallowable expense. In other words, added back as an expense for tax reasons and replaced with a claim for capital allowances instead.

6. Capital Allowances v Annual Investment Allowance

The annual investment allowance permits businesses to deduct 100% of the first £1,000,000 of their qualifying spend on plant & machinery against their taxes. This is instead of using capital allowances which permits a write off of typically 18% each year and applies to both Limited Companies and the self-employed.

The annual investment allowance is a type of capital allowance, but it only applies to equipment not cars. You could still use capital allowances on equipment you buy. However, this would restrict the amount you can claim against your taxes to 18% of cost each year. The AIA is more tax advantageous because it lets you claim 100% of what you’ve bought in the year you buy it.

7. What is the Capital Allowances Super Deduction?

The HMRC super deduction is only available for Limited Companies not Self-Employed

The capital allowances super deduction has been introduced to encourage spending as the UK recovers from the Coronavirus pandemic. From 1 April 2021 to 31 March 2023, businesses can claim 130% capital allowances on qualifying plant & machinery.

7.1 Example of the HMRC Super Deduction

A Company spends £200,000 on qualifying plant & machinery and is eligible to claim the HMRC super deduction for capital allowances. The business can claim £260,000 (£200,000 x 1.3) as an expense against its taxable profits. This means it will save tax when calculating its tax bill. So, if it pays corporation tax at 19%, it will save £49,400 on its corporation tax bill, instead of £38,000.

Related: