Disallowable expenses are things you can’t put on your tax return to reduce your tax bill. But which ones are those?

In this guide, I’ll explain what expenses you can’t put against your taxes (even if you consider them a business expense) and how to handle them when it comes to filling in your tax return.

This guide is for individuals who are registered as self-employed. Different rules apply if you have a Limited Company and pay corporation tax.

Friendly Disclaimer: Whilst I am an accountant, I’m not your accountant. The information in this article is legally correct but it is for guidance and information purposes only. Everyone’s situation is different and unique so you’ll need to use your own best judgement when applying the advice that I give to your situation. If you are unsure or have a question be sure to contact a qualified professional because mistakes can result in penalties.

1. What are Disallowable Expenses?

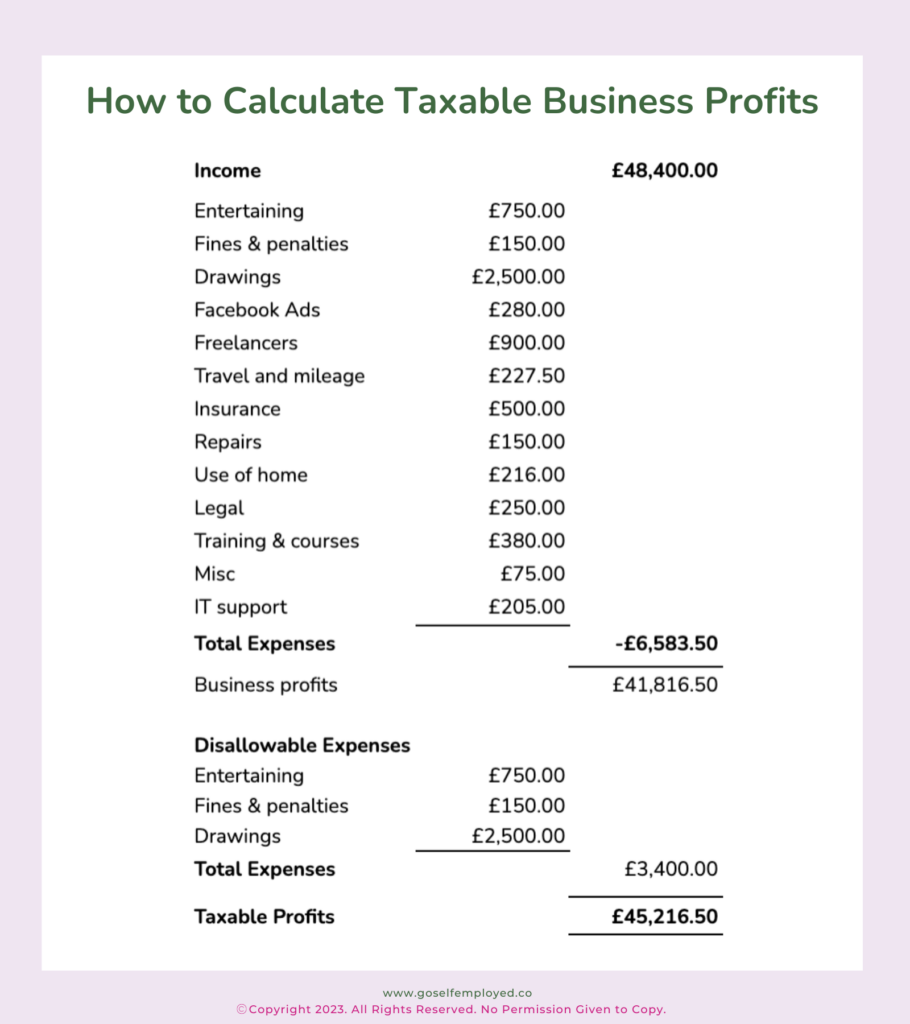

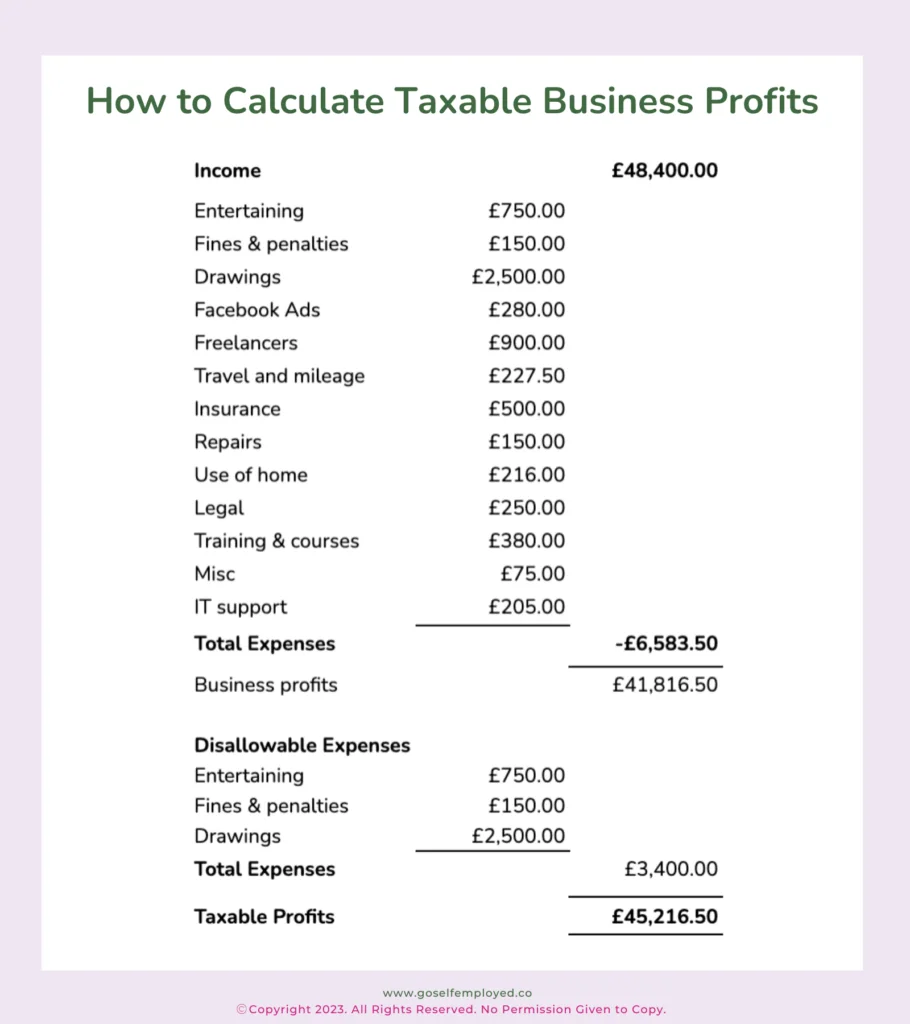

Disallowable expenses are things that you pay for but cannot be claimed as a tax deduction, even if you feel they were paid for as part of running your business.

If you’re confused about how expenses reduce your tax bill, then read this guide to self-employed tax to learn more about how taxable business profit is calculated.

Allowable expenses are things you can claim against your business income to reduce your tax bill. Read this guide to learn about allowable expenses for sole traders.

2. Examples of Disallowable Expenses

Here are some common HMRC disallowable expenses:

2.1 Travel from Home to Your Office

If you have chosen to rent an office or space from which to base yourself then any travel between your home to your office is not an allowable business expense.

If you are claiming business travel, read this guide to learn about which journies you can claim as a business expense

2.2 Client Entertainment

It may be entirely work-related but client entertainment is a disallowable expense. There are circumstances where you can buy a gift for your clients and can claim this as an allowable expense. However, if you take them out for a meal, even if it is to win a new contract or secure a business relationship, these costs cannot be claimed as an expense against your taxes.

2.3 Fines and Penalties

Any fines and penalties that you pay are a disallowable expense. That includes things like:

- Self Assessment Penalties

- Parking Fines

- VAT Penalties

2.4 Clothing

There are certain circumstances where someone who is self-employed can claim clothing on their tax return. This is because clothing is an allowable expense if it is:

- a uniform;

- protective clothing that you need for your work;

- costumes because you are an actor or entertainer.

Any other types of clothing will most likely be considered a disallowable expense. This would include everyday clothing or business suits.

2.5 Lunches

Read this guide to find out more details about claiming for clothing when you’re self-employed.

Everyday lunches cannot be claimed as an expense against your self-employment taxes. But, if you are out and about, away from your normal place of work, then you may be able to claim for your lunches.

You’ll find more details about claiming meals and subsistence in this food guide.

2.6 Training for New Skills

Whilst you can expense any training you do to improve your skills and keep you on top of your game. Training costs for learning new skills are a disallowable cost. However, you may be able to claim these when you set up your new business.

2.7 Salary

For those that are registered as sole traders, any salary paid to themselves is a disallowable expense. You are taxed on your income as whole, regardless of how much you pay yourself.

3. Handling Disallowable Expenses on Self-Assessment Tax Returns

Disallowable expenses cannot be claimed against self-employment taxes and incorrect claims can result in HMRC penalties.

Disallowable expenses can simply be excluded when filling in a tax return, whether total expenses are being entered as a single figure in the short-form self-employment section or as a breakdown.

Related: