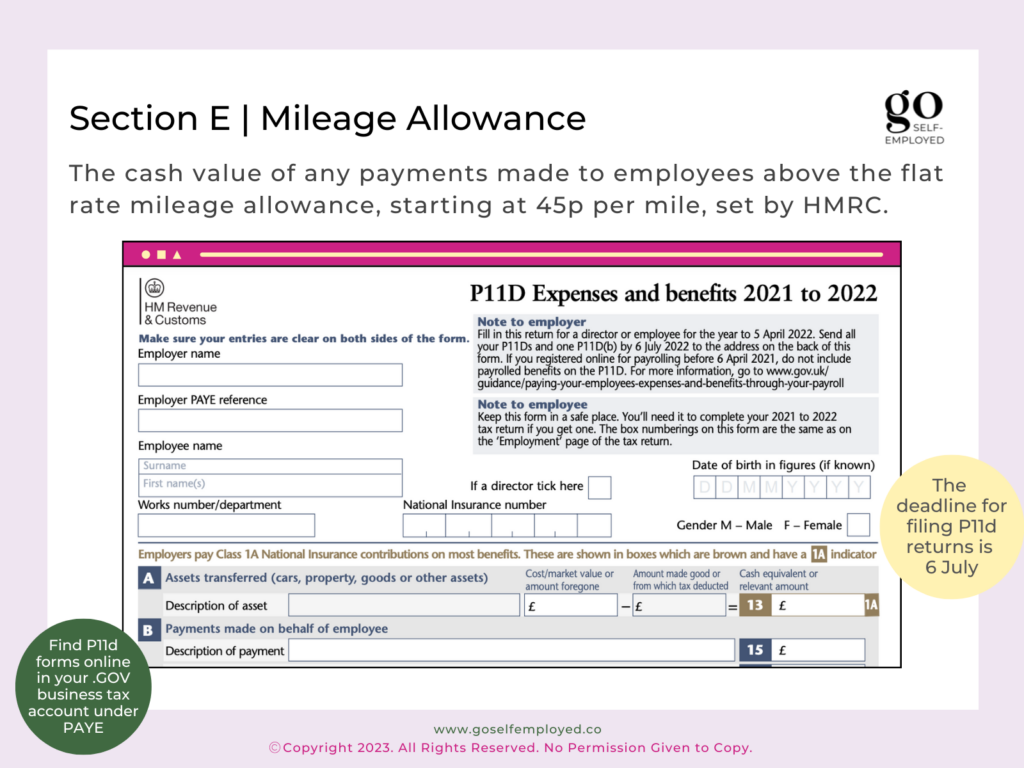

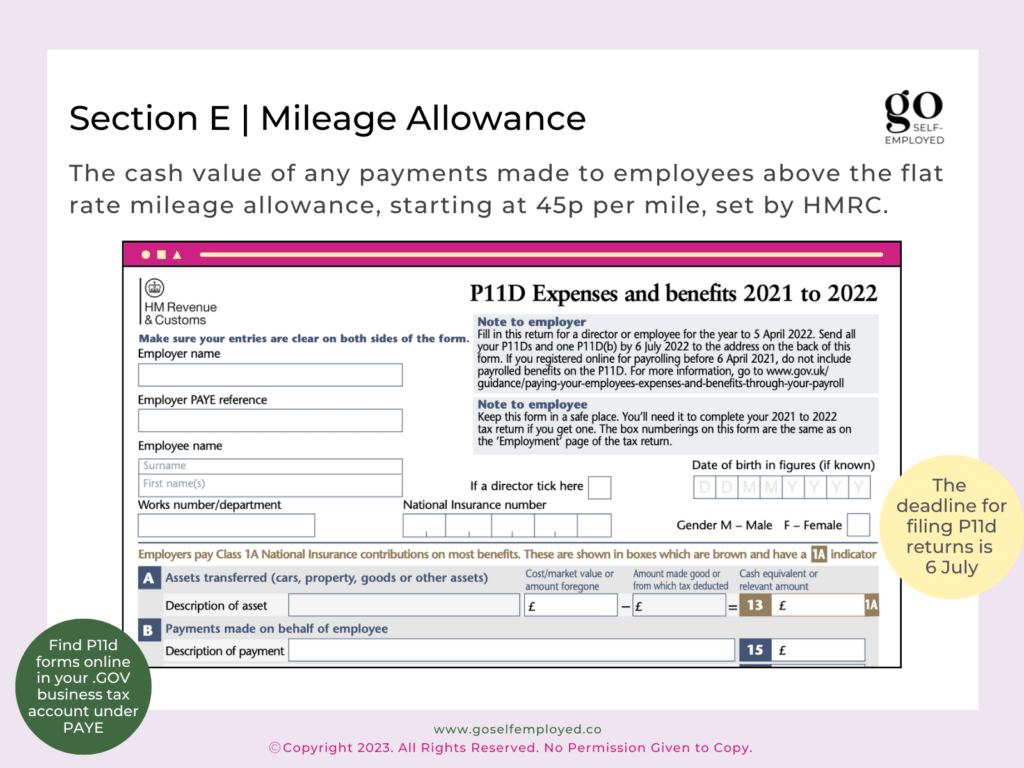

Section E of the P11d form covers the cash value of payments made to employees above the flat rate mileage allowance, starting at 45p per mile, set by HMRC.

Friendly Disclaimer: Whilst I am an accountant, I’m not your accountant. The information in this article is legally correct but it is for guidance and information purposes only. Everyone’s situation is different and unique so you’ll need to use your own best judgement when applying the advice that I give to your situation. If you are unsure or have a question be sure to contact a qualified professional because mistakes can result in penalties.

What are P11d Mileage Allowance Payments

Mileage allowance payments are HMRC-approved amounts Directors and employees can claim as an allowable business expense for business miles travelled in personal vehicles, whilst remaining free from any additional tax and NI.

The mileage allowance rates 2022-23 tax year:

- 45 pence per mile for cars and goods vehicles on the first 10,000 miles travelled (25 pence over 10,000 miles)

- 24 pence per mile for motorcycles

- 4p per mile for fully electric cars

The mileage rates set by HMRC are set at a rate per mile that contributes to the cost of wear and tear on a vehicle as well as fuel, MOT and servicing.

Where employees or Directors are paid rates in excess of the above, the amounts need to be included in section E of the p11d form. Income tax is then payable by the employee, although no additional tax is payable by the employer on the P11d(b) form.

Where Mileage Allowance Payments are made either equal to or less than the approved HMRC rates then no entry needs to be made in section E. But employees who received less than the approved rates can claim a tax refund on the underpayment as a work mileage tax rebate.

Related: