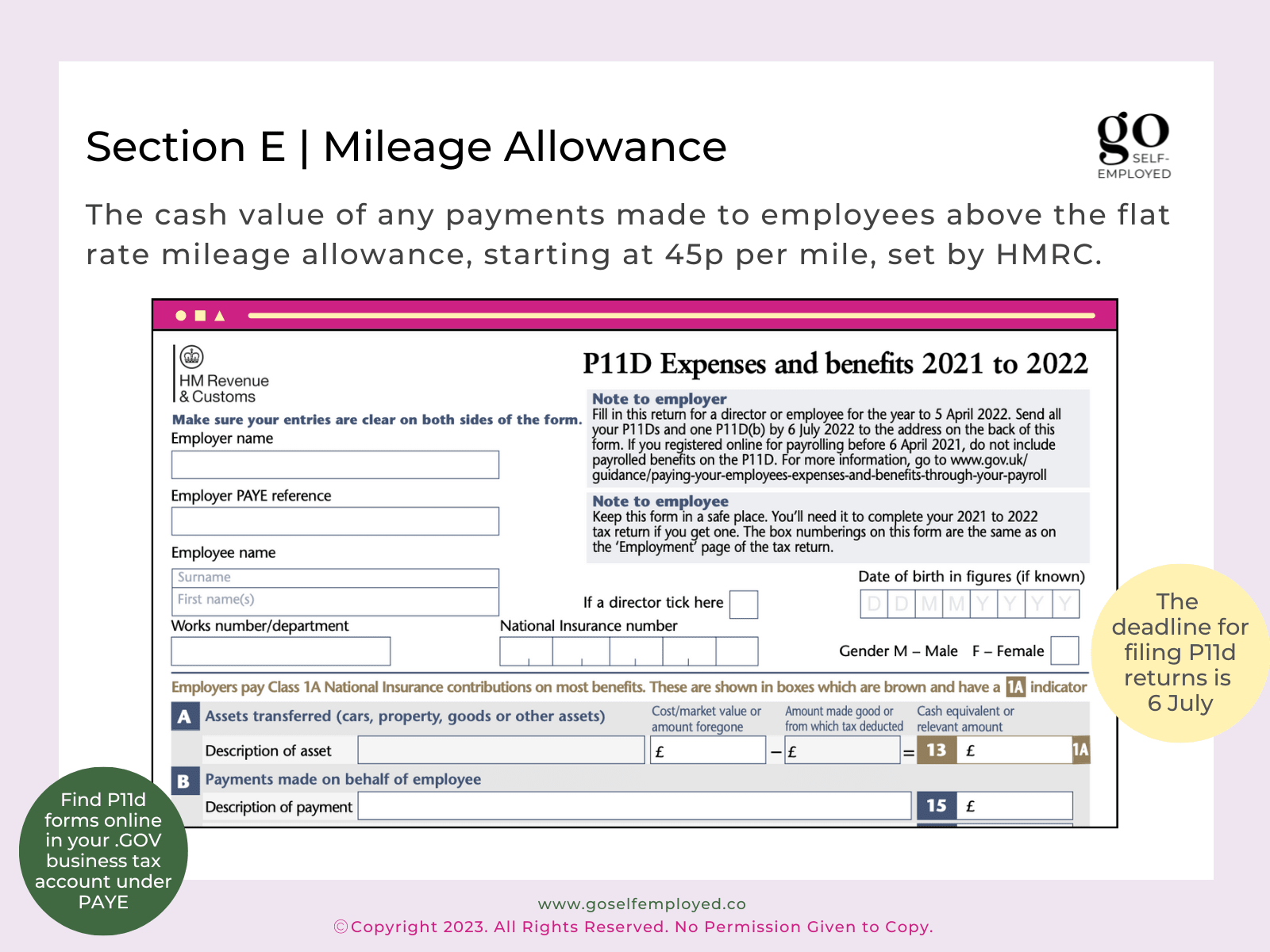

Section E – Mileage Allowance – P11d

P11d Mileage Allowance Section E should contain the amounts of any excess mileage allowance payments made.

When employers provide their employees with certain types of benefits, extra tax needs to be paid on the cash value of the perk provided. Here you’ll find out how tax is paid on benefits and how to report to HMRC using P11d forms.

Understand HMRC benefit in kinds (BIK), what counts as a taxable benefit for payroll (along with examples) and exemptions available for certain types of expenses that can be provided tax-free.

Get to know P11d and P11d(b)forms, which employers need to submit to HMRC with details of benefits provided and what information is contained on them.

P11d Mileage Allowance Section E should contain the amounts of any excess mileage allowance payments made.

P11d Section D Living Accommodation relates to the cash equivalent of any payments made for living accommodation provided to employees.

Section C of the P11d form covers the cash value of payments made to employees in the form of vouchers or via company credit cards for personal expenses by the employer.

P11d Section B Payments Made on Behalf of the Employee relates to any amounts that should have been paid by an employee but were paid by the business instead.

Section A – Assets Transferred – covers the cash value of assets transferred from an employer to an employee or director.

Section F of the P11d form covers the cash value of company cars and fuel provided to employees that they use personally, as well as for work reasons.