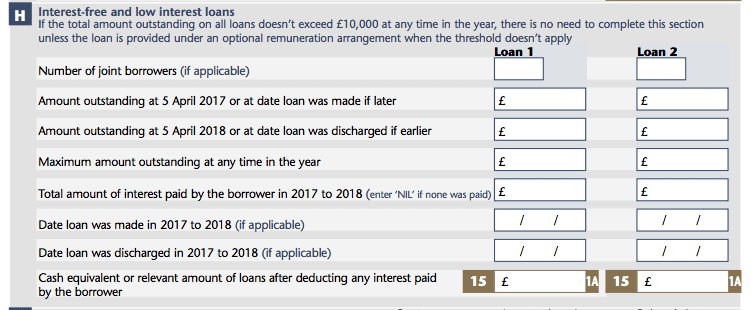

P11d Loans Section H: Interest and Low Interest Loans. This section covers details of any loans made to employees and Directors at a beneficial rate of interest or under beneficial loan terms.

Whatever the reason, employers commonly help their employees out by giving them loans at a beneficial rate of interest. That means making a loan at an interest rate set at a lower amount than what you would typically see on the open market.

Such transactions are classified as P11d loans, with tax payable on the beneficial rate of interest.

P11d Loan Exemptions

Certain loans are not considered P11d loans – these are known as “qualifying loans”.

A qualifying loan is one that does not attract any additional tax or national insurance and does not need to be disclosed on a P11d form.

These include:

- non-business loans made in the normal course of a domestic or family relationship as an individual (not as a company you control, even if you are the sole owner and employee);

- loans made to employees which have a total combined outstanding value to an employee of less than £10,000 throughout the whole tax year (£5,000 for 2013 to 2014);

- loans made to employees at a fixed and invariable interest rate that was equal to or higher than HMRC’s official interest rate (2.5% for 2017/2018) when the loan was taken out;

- the terms of any loans are identical to terms and conditions of loans made to the general public by a commercial lender;

- loans that are ‘qualifying loans’, meaning all of the interest qualifies for tax relief (such as a loan to purchase an interest in a partnership or commercial loans);

- using a director’s loan account as long as it’s not overdrawn at any time during the tax year.

Calculating the Cash Value of a P11d Loan

The cash value of the loan needs to be determined by using an averaging method and HMRC provides a worksheet to help you work out the cash equivalent.

Here are the 10 steps you need to go through the calculate the cash equivalent.

| Step | Calculation |

| 1 | Maximum balance on either 5 April 2018 or the date the loan was taken out (whichever was later) |

| 2 | Maximum balance on earlier of day loan was discharged or 5 April 2019 |

| 3 | Total (step 1+step 2) |

| 4 | Divide step 3 by 2 |

| 5 | Number of complete tax months in the tax year throughout the loan was owing |

| 6 | Multiply step 4 by step 5 and divide by 12 |

| 7 | Official rate of interest |

| 8 | Multiply step 6 by step 7 |

| 9 | Enter interest paid in 2018/2019 |

| 10 | Cash equivalent of loans step 8 minus step 9 |

Who Pays Tax on P11d Loans

Tax on interest and low interest loans in Section H is paid by the employee and Class 1a National Insurance is payable by the employer.