The SA102 form is one of the supplementary sections to the SA100 tax return form. This form is used if an individual has employment income that needs to be declared to HMRC as part of self-assessment.

Table of contents

1. What is an SA102 Form?

SA102 is the name given by HMRC to the employment page of the tax return, used by those completing a paper return. For those filing their tax return online, they won’t see this code name, but it is essentially the same form and will appear if an individual ticks the box “Were you an employee (or director or officeholder) or agency worker in the year to 5 April 2021?”.

It is commonly used to capture tax payable on employment benefits such as a car or healthcare, where this hasn’t been deducted at source. Or to calculate an accurate income tax bill for individuals who have multiple sources of income, since income tax is a cumulative type of tax and the more someone earns the more they pay. For example, someone who is employed and self-employed will pay income tax on their combined income, so needs to enter their employment income so the tax they owe is calculated correctly.

The SA102 form only needs to be completed if applicable to the individuals situation, otherwise it can be ignored.

2. Who Needs to Complete an SA102?

If an individual is completing a tax return then they’ll need to fill in the employment page if they:

- work for an employer under PAYE, including agencies and umbrella companies;

- are a Company Director or hold a position such as a chairperson or treasurer;

- receive foreign income from a job or directorship;

- had an outstanding balance on a disguised loan from an employer or previous employer as at 5 April 2019.

One or more SA102 forms may need to be completed if the individual holds multiple jobs, directorships or positions.

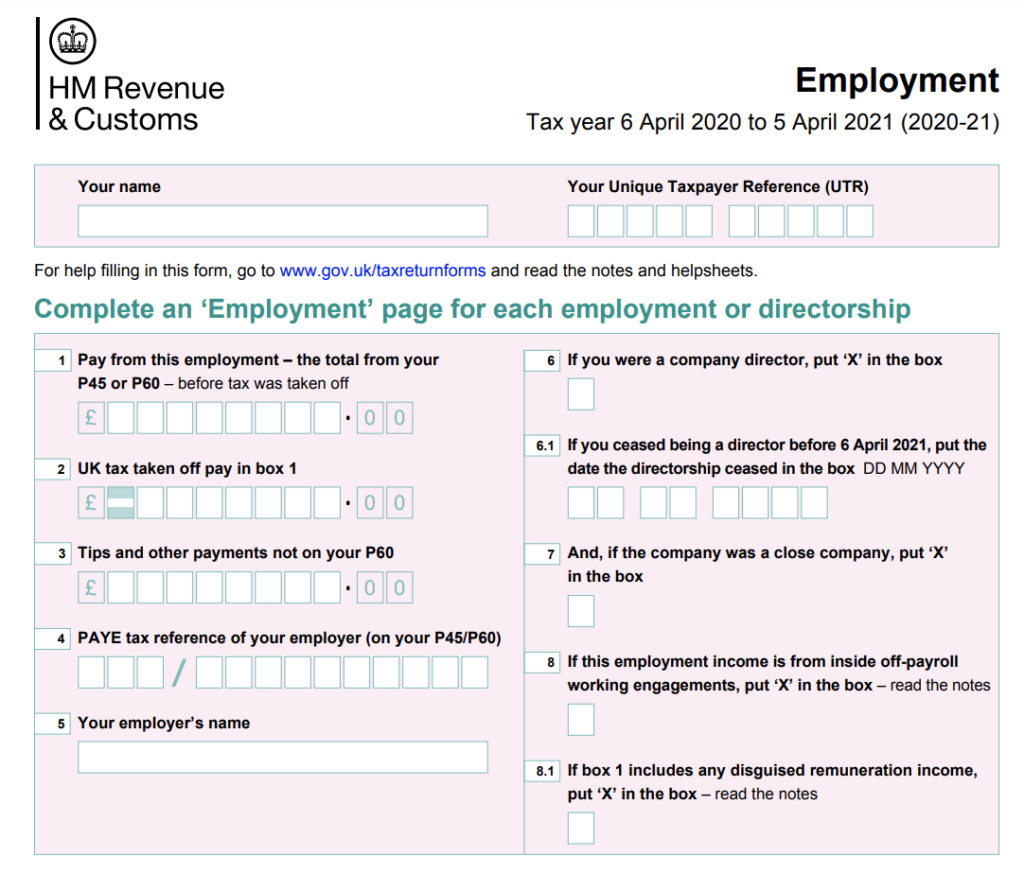

3. How to Fill in the Employment Page

Much of the information that needs to be included on this form can be found on the following tax forms:

The SA102 is split into three sections. In the first section details of pay and remuneration should be share, next are the boxes to declare taxable benefits received and finally there is a section to claim for employment expenses.

3.1 Enter Pay from Employment

Along with entering details of an individual’s pay and tax already deducted, HMRC also wants to know some important information that helps build a picture of how the person is earning their income and whether any adjustments need to be made for additional tax payable. This includes letting them know whether the person:

- Was the director of a close company;

- If they are working inside off-payroll, an evolution of the IR35 regulations;

- Whether they received any disguised remuneration income.

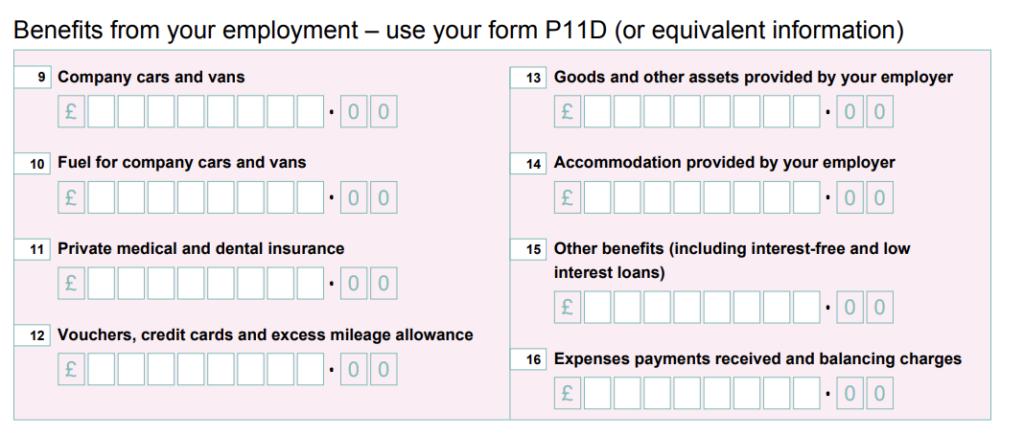

3.1 Enter Benefits from Employment

If an individual has received benefits from their employer, such as a company car or private healthcare and not paid tax on them, then they need to enter details of these here. That way, they will pay the right amount of tax on the cash equivalent of what they have received. The information on what they have received will be on their P11d form, which is issued by their employer.

Do not enter benefits that an individual has already paid tax on, for example, because their employer deducts tax through the PAYE system. Otherwise the individual will end up paying tax on these twice.

Information entered here can affect a persons tax code because HMRC may opt to amend their code so that tax is paid at source (in other words through payroll) instead of through the annual tax return.

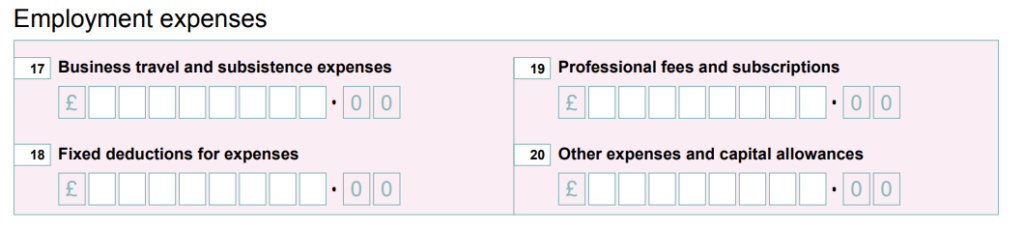

3.2 Claim Employment Expenses

If an individual incurs costs for their job, but these are not reimbursed by their employer then they can claim for them here (alternatively, if they are not registered for self-assessment they can fill in a P87 form).

Don’t forget individuals can claim mileage rebate if they are paid less than the HMRC approved mileage rate for using their personal vehicle for work reasons, but the person must keep detailed records of where they have travel and why.

Read this guide to understand more about claiming fixed deductions for expenses such as uniforms and working from home.