Are you ready to complete the employment page of your tax return? Are you confused by which boxes you need to fill out and what words like ‘close company’ or ‘office holder’ mean? Then look no further! In this guide, you’ll find out how to fill in the employment section whether you were full-time employed, part-time or working on a casual basis. And, I’ll explain how to claim extra employment expenses on your tax return.

Friendly Disclaimer: Whilst I am an accountant, I’m not your accountant. The information in this article is legally correct but it is for guidance and information purposes only. Everyone’s situation is different and unique so you’ll need to use your own best judgement when applying the advice that I give to your situation. If you are unsure or have a question be sure to contact a qualified professional because mistakes can result in penalties.

Table of contents

1. Who Needs to Complete the Employment Page?

You need to fill in the employment section if you were employed either full-time, part-time or on a casual basis by someone. This includes if you have a Limited Company and pay yourself via your payroll. If you had more than one job during the tax year, you are doing your self-assessment for, you’ll need to fill out more than one employment section. You should have let HMRC know this in the tailor your return section, when you signed into your .GOV account with your HMRC user ID.

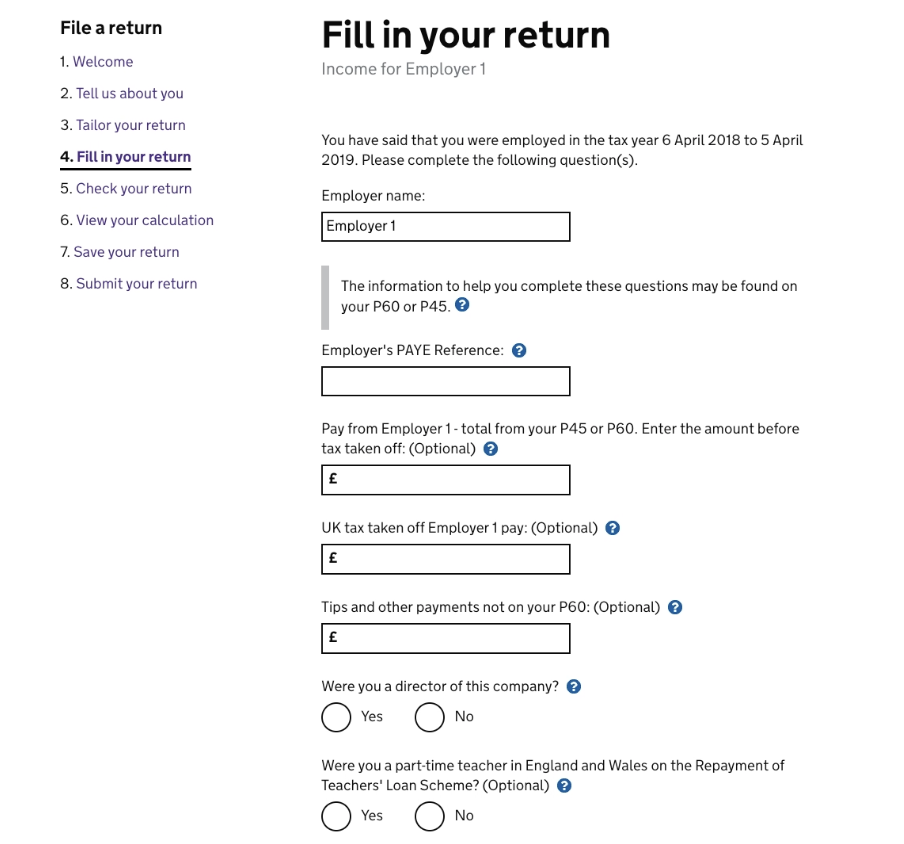

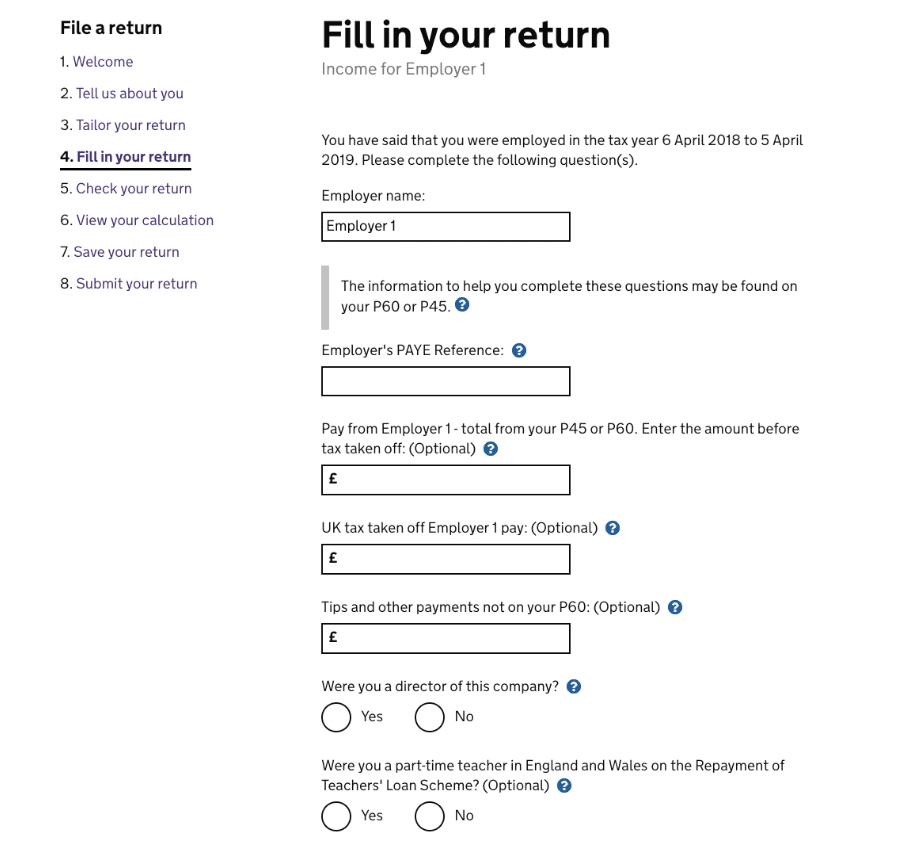

2. How to Complete the Employment Page of Your Tax Return

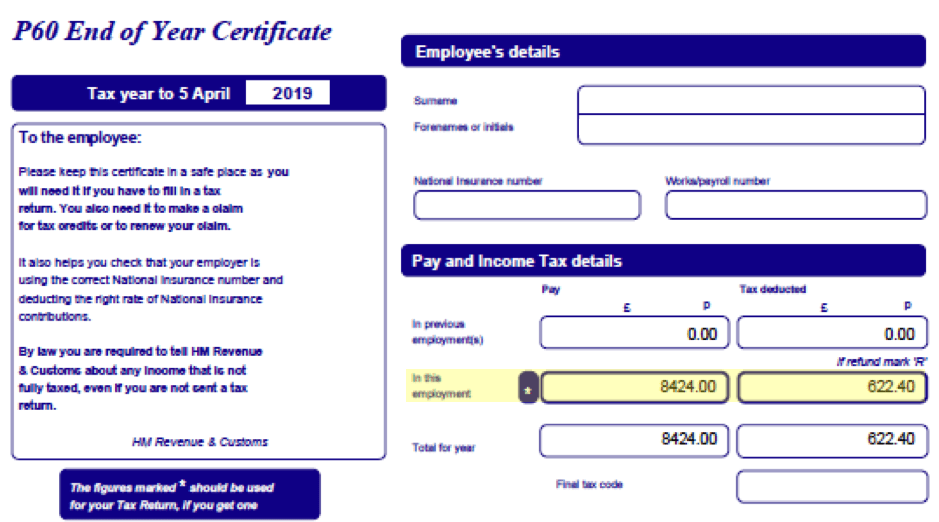

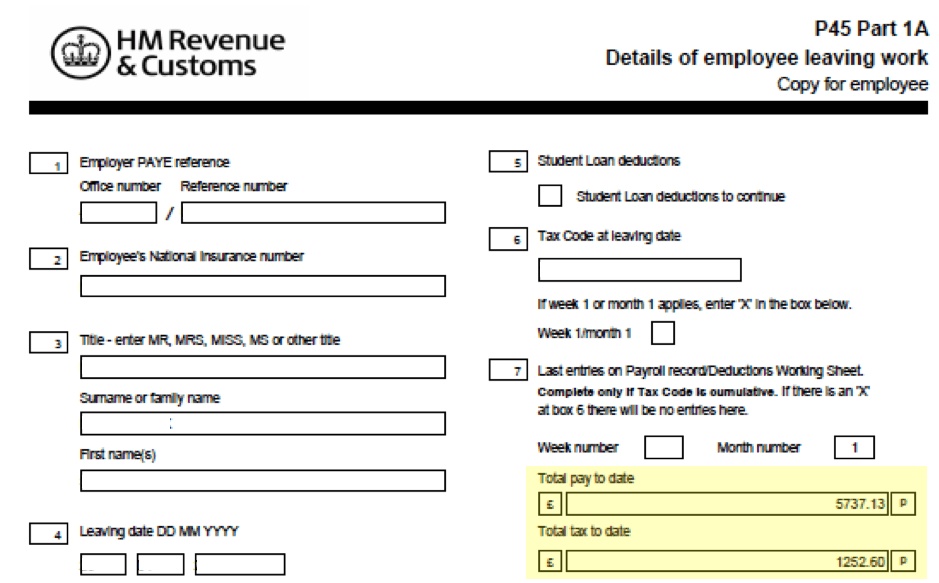

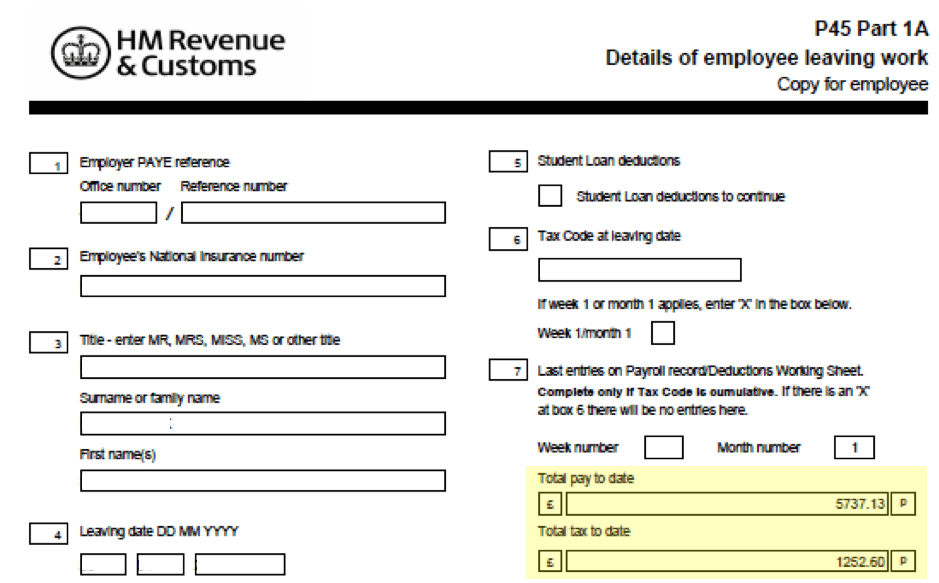

You’ll need to enter your Gross Pay from your job (that’s the amount before any income tax was deducted). You also need to confirm your employer’s name and any benefits in kind you have received. You’ll be able to find all this information will be on your:

The areas highlighted in yellow below show where you can find your gross pay and tax deducted on your P45 or P60.

Remember:

- You don’t need to include National Insurance deductions, just income tax deducted;

- If you were paid any tips, cash in hand money or other payments that were not included in your P60, you’ll need to enter them in this section;

- You’ll need to include taxable benefits paid to you by your employer, these will be on your P11d.

3. What is a Close Company?

If you are the director of a Limited Company, then you’ll need to disclose whether it is a close company on your SA100 tax return. A Close Company for UK tax purposes is a Limited Company that has 5 or less participators or where all the participators are also directors. For most small Limited Companies, participator means shareholder. However, it can also apply if a Company has certain types of borrowing or creditors like debentures. So, if you are the sole Director and shareholder of your own Limited Company, then you need to choose “yes”.

The rules around Close Companies can be complicated, so always consult a professional if you are unsure how to answer this question.

4. Claiming Tax Relief on Your Job Expenses

If you paid for certain business expenses as part of your job but were not reimbursed for them by your employer, then you may be able to claim tax relief on what you have paid in this part of your online tax return, if you haven’t claimed these with a P87 form. One of the most common expenses is working from home due to Coronavirus, but you can also claim things like:

- business travel including incidental meals, accommodation and mileage for using your own vehicle for work reasons;

- flat rate expenses that cover the costs of maintaining or replacing tools, uniforms or special work clothes;

- professional fees and subscriptions;

- capital allowances for buying large items of equipment necessary to do your job (but not cars or vans).

To claim for any employment expenses or capital allowances for equipment used in your employment, please make sure you select ‘Yes’ from the drop-down menu in the employment page of a tax return; otherwise, select ‘No’. You can only deduct the costs you had to pay out in doing your job that meet the HMRC criteria. You cannot claim for personal expenses.

4.1 Business Travel and Subsistence Expenses

If you have paid for business travel and incidental costs you can claim this here. Generally, you can claim the cost of:

- Travel but not your normal commute;

- Related food costs, keep your claim reasonable;

- Accommodation;

- Mileage allowance to cover the cost of using your own car, motorcycle or bike (make sure you use the set rates below and keep a record of how you reached your claim);

- Additional mileage if your employer pays you less than the HMRC set rates below;

- Other expenses like using your phone calls.

[table id=7 /]

You’ll need to add up the amounts you have spent in respect of travel and subsistence, then include them in the first box.

4.2 Fixed Deductions for Expenses

HMRC allows you to claim tax relief if you are responsible for paying for cleaning, maintaining or replacing:

- Specialist work clothes, like nurses uniforms, hard hats and safety boots;

- Occupational uniforms if you are an NHS worker for example or a member of the police force;

- Small tools like an electric drill.

You can only claim for the cost of replacing an item, not the initial cost of buying it, claiming either:

- The actual amount you have spent, but you will have to keep receipts;

- The flat rate as set by HMRC.

4.3 Professional fees and subscriptions

You can claim tax relief on professional fees and subscriptions for approved professional organisations only. However, not all fees and subscriptions are eligible. You can check whether what you’ve paid for meets the criteria for HMRC approval here.

4.4 Other expenses and Capital Allowances

You can include in this box any amounts you have paid for buying small items of equipment that you need to do your job, but your employer did not provide for you. So, that’s things like electric drills or a mouse for your laptop.

You can claim for more expensive items, like a laptop, but you’ll need to claim tax relief using capital allowances. You cannot claim cars or vans in this way.

Claiming expenses is strictly reviewed by HMRC and it is common to find mistakes on claims. Therefore, if you are planning to claim tax relief on expenses make sure everything you have paid for is truly eligible, you have receipts where necessary and you do not claim for anything your employer has reimbursed you for.

5. Changes to Your Tax Code

If you delcare P11d benefits in kind or choose to claim for expenses in this section of your self assessment tax return, then you should be aware that HMRC may adjust your tax code. That means you may see a change to your net pay on your payslip.

Once you submit your tax return, HMRC sometimes makes the assumption that your tax will be the same for the upcoming tax year and choose to change your tax code (without your consent). That means you could end up paying more income tax throughout the year, in particular, if you receive taxable benefits in kind and could be owed a tax refund.

Related: