Understand how tax works if you’re employed and self-employed, what you need to check on your payslip and what you have to tell HMRC about.

Friendly Disclaimer: Whilst I am an accountant, I’m not your accountant. The information in this article is legally correct but it is for guidance and information purposes only. Everyone’s situation is different and unique so you’ll need to use your own best judgement when applying the advice that I give to your situation. If you are unsure or have a question be sure to contact a qualified professional because mistakes can result in penalties.

Can You Be Employed and Self-Employed at the Same Time?

Yes you can be employed and self-employed at the same time. It’s very common to find individuals running a business while working full time especially while they are growing their business or are just starting self-employment.

If you are planning to be employed and self-employed at the same time then you should check your employment contract in case it prohibits you from being self-employed, although you may want to consider telling your boss about your side hustle.

Whether you choose to tell them or not it is probably a good idea not to tread on your employer’s toes, for example, by stealing clients or working on your side hustle during work time which could jeopardise your full-time job.

Tax When You’re Employed and Self-Employed

If you look at your payslip, you’ll see that your employer has paid you after deducting income tax and national insurance. You’ll be paying these taxes under the PAYE system and in most cases you won’t hear from HMRC, except in the unlikely event you are on the wrong tax code and are owed a tax refund.

When you work for yourself the money you are paid has no tax deducted from it. When you’re self-employed you are responsible for working out how much tax and national insurance you owe, paying them over to HMRC in accordance with the rules of self-assessment.

What is Self-Assessment?

Self-assessment is the process created by HMRC that allows anyone who receives untaxed income to declare it to the government and pay any tax due.

When you are self-employed, either part-time or full-time because the money you are paid is taxable income, it’s your responsibility to tell HMRC about it and work out how much tax you owe. The way you do this is by registering for self-assessment to fill in a tax return.

What is a Tax Return?

A tax return is a form issued by HMRC (also known as an SA100). It contains lots of different sections and boxes that you need to fill in to declare your income. Once completed, HMRC will then calculate how much tax you owe ready for you to pay them.

You need to fill in your tax return by the 31 January each year summarising all your earnings for the previous tax year. The tax year runs from 6 April to 5 April each year. So a tax return due by 31 January 2023 would contain earnings between 6 April 2021 to 5 April 2022.

If you are employed and self-employed you’ll need to fill in two sections of the return:

- Employment section with details of your employer, gross income and tax deducted

- Self-employment section with details about your business, income and expenses

You’ll also need to fill out more sections if you receive other types of taxable income like rental income and dividends.

How Much Tax Do You Pay When You’re Employed and Self-Employed

When you’re self-employed you’ll pay income tax, Class 2 and Class 4 national insurance on your business profits. Profit means all your business turnover minus expenses you can claim as a tax deduction.

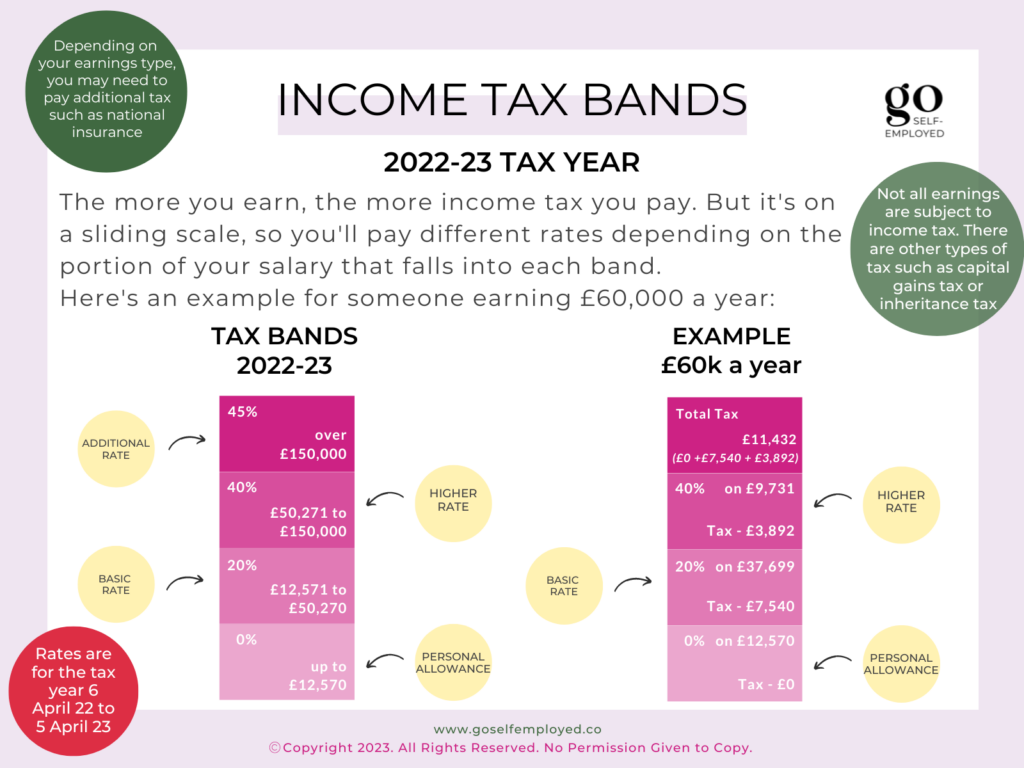

Income Tax

Income tax starts at 20% on all your income (not just from self-employment) over £12,570, 40% over £50,270 and 45% on everything over £150,000. It is a cumulative tax which means the more you earn the more you pay. Therefore, when you are employed and self-employed, you’ll pay income tax based on all your taxable income.

So say, if you are employed on a salary of £25,000 and have business profits of £20,000, you’ll pay income tax of £6,486 based on your combined income of £45,000, worked out as:

£12,570 x 0% = £0

£32,430 x 20% = £6,486

The first £12,570 of income is tax-free since it is covered by the personal allowance. When you are employed and self-employed, it’s really important that you only claim this allowance once otherwise you’ll end up owing HMRC money back.

To avoid this problem, you should check your payslip and find your tax code. The most common tax code in use for 2022/2021 is 1257L. This means your employer will be giving you a portion of your tax-free allowance every time they pay you unless you find yourself on an emergency tax code such as BR or 0T.

If you have used all your personal allowance up in your employment, then all your self-employment profits will be taxed at 20% or more. If you haven’t used up all your personal allowance, you’ll get credit for any unused amounts when you fill in your tax return.

National Insurance

In addition to income tax, you’ll also pay two types of national insurance on your self-employed profits – class 2 and class 4.

Class 2 national insurance is paid as a set weekly amount of £3.15 on profits over £6,725. Class 4 is worked out as 9% on profits between £9,880 to £50,270 and 3% thereafter.

Class 2 and class 4 national insurance are not related to your other income. It’s a charge on your business profits only.

You’ll be paying Class 1 National Insurance on your employment earnings which you can find on your payslip. However, you’ll also need to pay Class 2 and Class 4 National Insurance on your self-employment profits which isn’t connected to your employment earnings.

Following on from the example above, we can ignore employment earnings of £25,000 for the purposes of calculating Class 2 and Class 4 National Insurance, and just calculate it on the £20,000 business profits. Here’s how it’s worked out:

- Class 2 National Insurance £163.80 (£3.15 x 52 weeks)

- Class 4 National Insurance £1,037.30 (£20,000 – £9,880 x 10.25%)

When you are employed and self-employed, you pay three types of national insurance – Class 1, Class 2 and Class 4. You can apply to reduce your Class 4 National Insurance payments under the rules of the HMRC annual maximum.

When Should You Register as Self-Employed?

You’ll need to register as self-employed once your business income (not profit) goes over £1,000. Below this, you can choose to take advantage of the £1,000 trading income allowance.

The deadline for registering is the 5th October following the end of the tax year you started working for yourself or your income goes over the £1,000 limit.

There are other business structures out there including a Limited Company which may offer better tax savings depending on your earnings. You can find out about the most popular UK business structures in this guide.

Related: