If your payslip shows the UK 1250l tax code, then you’re on one of the most commonly used tax codes for the 2020-21 tax year. In this guide, I’ll explain more about what the tax code 1250l means and why it’s used. I’ll also show you how to check your tax code is correct.

Friendly Disclaimer: Whilst I am an accountant, I’m not your accountant. The information in this article is legally correct but it is for guidance and information purposes only. Everyone’s situation is different and unique so you’ll need to use your own best judgement when applying the advice that I give to your situation. If you are unsure or have a question be sure to contact a qualified professional because mistakes can result in penalties.

1. What UK Tax Codes Mean

A tax code is a numerical number followed by a letter, that is issued by HMRC to your employer. Your employer uses it so they know how much income tax they need to deduct from your salary. HMRC have to issue it because they have all the information on your personal income and any deductions they need to take from you. This means you can keep things confidential from your employer.

Your tax code lasts for one tax year. Therefore, both you and your employer will most likely receive a coding notice before the start of a new tax year. You and your employer may also receive a letter from HMRC to change your tax code if your circumstances change, for example, if:

- you are claiming the marriage allowance tax rebate

- need to pay the £50,000 high-income tax charge

- are self-employed and want to pay any tax you owe through your PAYE tax code

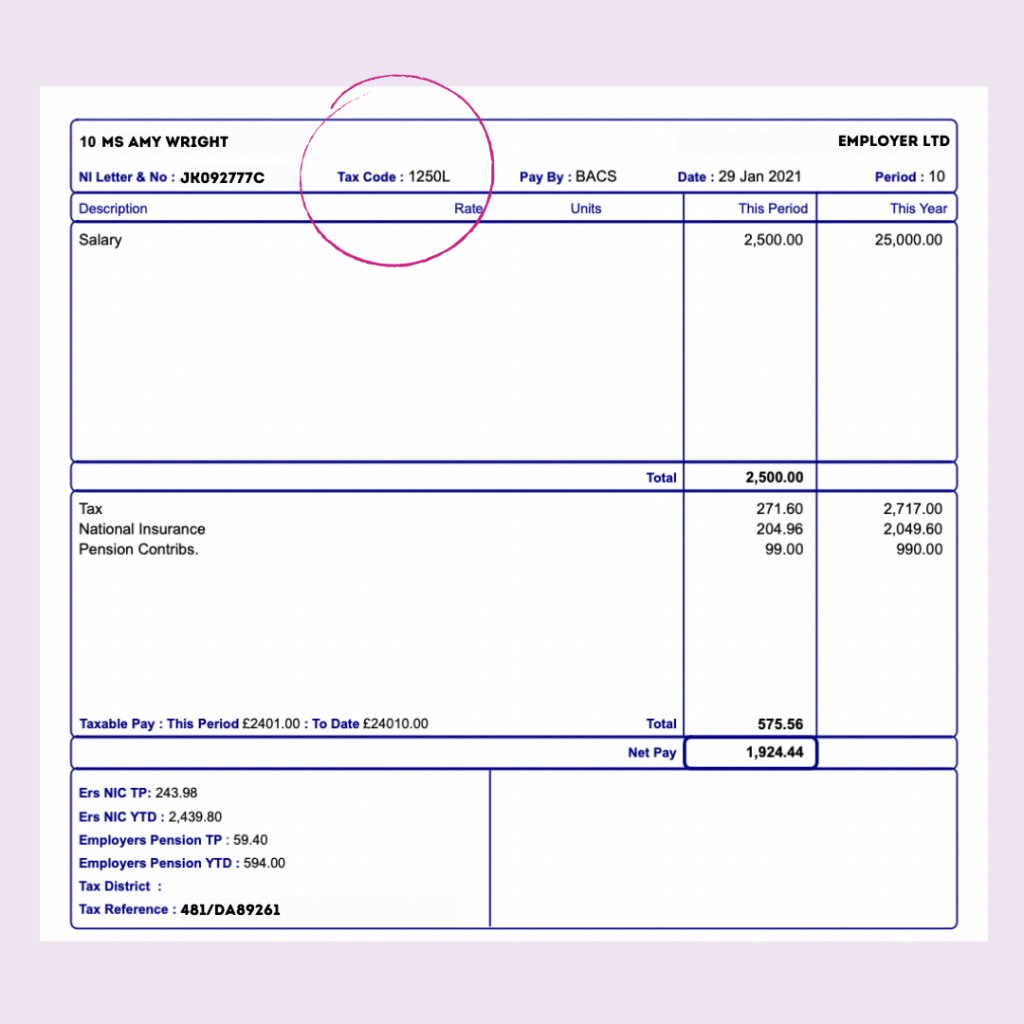

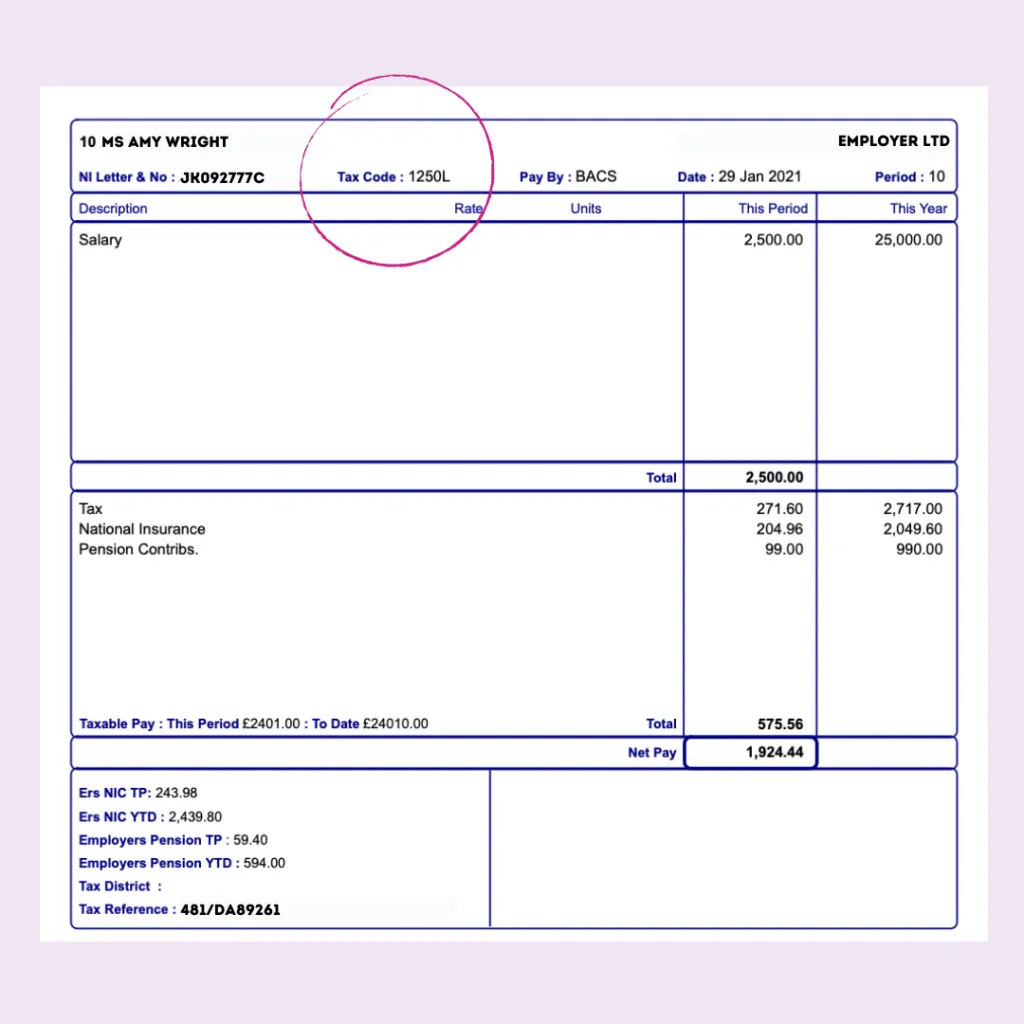

2. What Does the 1250l Tax Code Mean?

Each code tells your employer how much tax to deduct. The tax code 1250L is used by people with one job and no work benefits like a company car or one pension.

Every year, all UK residents are entitled to earn an amount tax-free known as a personal allowance. For both the 2019/2020 and 2020/2021 tax years, this is £12,500. After this, you’ll pay income tax at 20% on your earnings up to £50,000 and 40% over that amount, until you reach £150,000 and have to pay 45%.

[table id=2 /]

For the purposes of tax coding, HMRC removes the last digit and replaces it with a letter. In this case, the letter “L” has been used which means you’re entitled to the standard tax-free Personal Allowance.

3. Why Did Your Tax Code Change from 1185L to 1250L?

The Personal Allowance in the tax year 2018/2019 was £11,850 but it has since changed to £12,500. It means you are entitled to more tax-free pay and the change in your tax code from 1185l to 1250l ensures your employer passes your tax-free pay onto you.

4. 1250l Cumulative Tax Code

The tax code 1250L is a cumulative code. You’ll sometimes see it written as 1250l Cumul. It means you’ll receive a portion of your Personal Allowance every time you get paid. For example, if you are paid monthly, you’ll receive £1,041,67 (£12,500 ÷ 12) tax-free each month you get paid. That way by the end of the tax year, you’ll have received your Personal Allowance in full.

If you took a few months of work and had no other job during the tax year, you’ll receive all the Personal Allowance you are owed in your first payslip if you start a new job. Your employer will know what code to use when you give them your P45.

If your tax code ends W1 (week 1), M1 (month 1) or X, then you have been put on a non-cumulative or emergency tax code.

5. Emergency Tax Codes 1250W1, 1250LM1, 1250X

If you have the 1250W1, 1250LM1 or 1250X tax code, then you’ve been put on an emergency tax code. This normally happens if you:

- start a new job and not provided a P45

- begin working for an employer after you’ve stopped self-employment

- receive company benefits, like a company car

- receiving the State Pension

Although emergency tax codes are temporary while the necessary information is put together, it does mean you’ll pay tax on all your income above the Personal Allowance and not receive any backlog of personal allowance you may be entitled to but haven’t used.

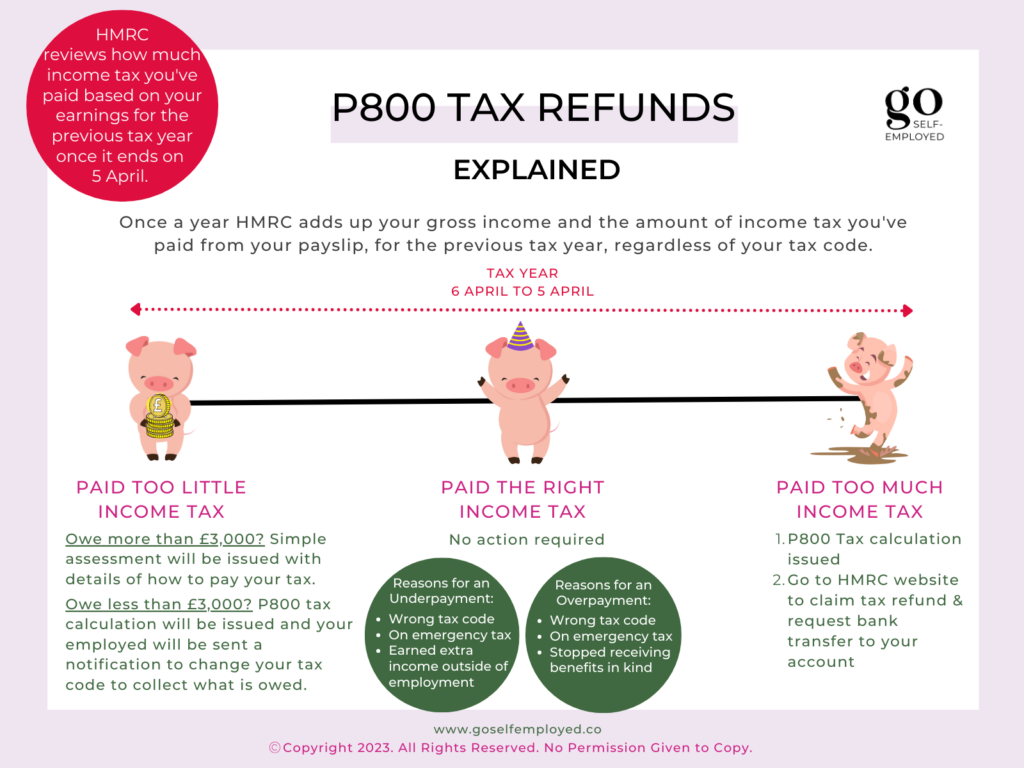

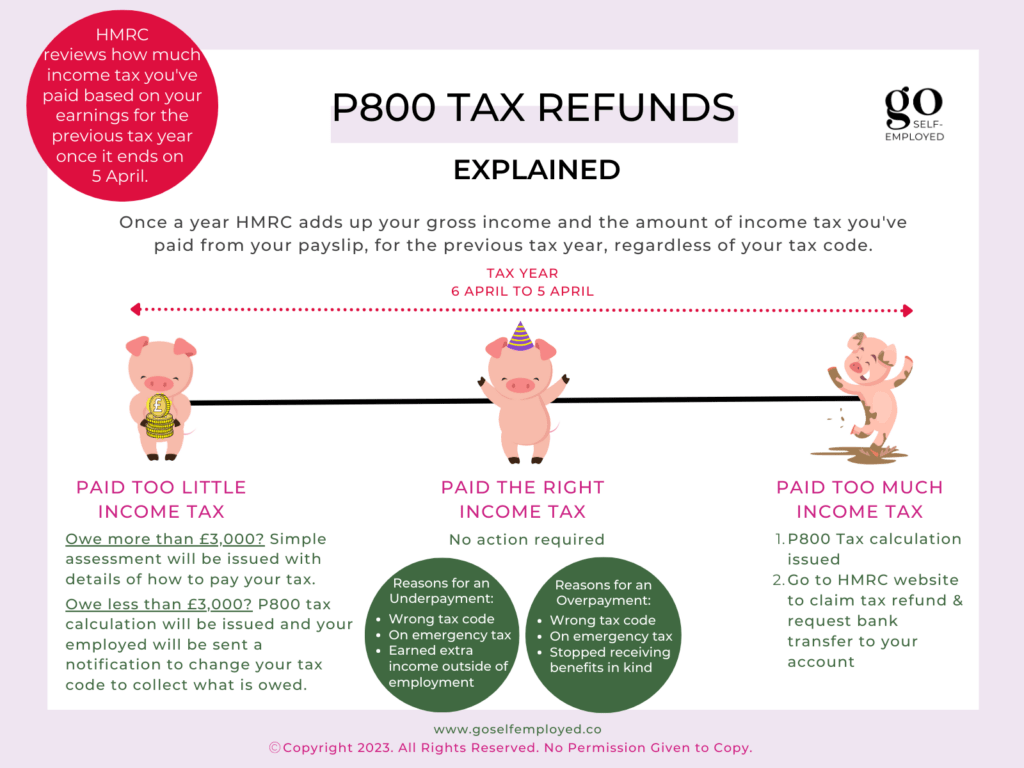

If you end the tax year on an emergency tax code, HMRC will add up how much tax you have paid and work out whether you owe anything at the end of the tax year. They will then send you an HMRC tax code notification letter called a P800 detailing what you are owed and how you’ll be repaid. If you are registered as self-employed, any money you are owed will be credited to your tax account.

6. How to Check If Your Tax Code Is Correct

If you think that you shouldn’t be on the tax code 1250L, then you can contact HMRC on 0300 200 3300. Alternatively, you can use the HMRC online checker, by logging into your Personal Tax Account.

Unfortunately, your employer may not be able to help you because they can only act on the information sent to them in the HMRC coding notice.

7. What Happens if You Haven’t Paid Enough Tax

If HMRC discovers, for whatever reason, that you have underpaid your tax during the year, they will recalculate your tax. They will then issue you with a P800 calculation if you owe less than £3,000 or send you a simple assessment letter if you owe more than £3,000.

8. Tax Code 1250L and Self Employment

If you work for yourself, you’ll have a UTR number which is a numerical number used by HMRC for managing your self-assessment information.

If you are employed and self-employed then you may have the 1185l tax code as well as a UTR number. It means, your employer is giving you your Personal Allowance. In this instance, it’s most likely that all the profit you earn from your business will be taxed at your highest rate of tax.

When you fill in your tax return online, you’ll have to declare all your income in the employment and self-employment sections of your tax return. But you’ll get credit for any tax you’ve paid in your employment when HMRC calculates your tax bill.

Related: